Budgeting Across Borders in 2025: What Actually Changes

Remote work erased office walls, not financial borders. In 2025, volatility in FX rates, real‑time payment rails, and country‑by‑country tax rules shape how you plan. Your budget now needs a currency layer, a tax‑residency layer, and a compliance layer. Think cash flow in base currency, then map income and bills by location and time zone. Automations help, but you still need a human check on fees and taxes. Aim for a portable setup: one source of truth for money, quick local rails for spend, and clear rules for saving and tax buffers.

Comparing Approaches: Pick a Method That Travels Well

Zero‑based budgeting gives control when income swings, but it’s time‑hungry. The percentage (50/30/20) model is lighter, yet can hide FX slippage. Bucket (envelope) budgeting works best across countries: create buckets by currency and purpose—rent, visas, flights, tax, emergency—and set target balances in your base currency. If you invoice irregularly, hybridize: zero‑base new income, then sweep fixed percentages to buckets. Add a rolling three‑month runway so a delayed client payment or border hop doesn’t nuke your essentials.

Tech Stack: Pros and Cons You Should Know

Aggregation apps now auto‑detect currencies and tag fees, while AI nudges flag expensive routes. The upside: fewer blind spots and faster reconciliations. The downside: data‑sharing risks, category mislabels, and subscription creep. Shortlist the best budgeting apps for digital nomads that support multicurrency, offline receipt capture, and tax tagging. Pair them with best no foreign transaction fee credit cards to dodge 2–3% FX markups. Keep a manual monthly review; automations are great at speed, not judgment when banks rename fees or change exchange spreads.

Accounts and Transfers: Make the Rails Work for You

For day‑to‑day spend, the best multi-currency accounts for digital nomads shine when they offer local account numbers, free ATM tiers, and mid‑market FX. Keep one “settlement” account in your earning currency, then convert just‑in‑time to pay bills. For moving funds, test routes quarterly; what was the cheapest international money transfer last year may not be now as providers tweak spreads. Set alerts for FX bands and pre‑fund when rates are favorable, but cap exposure—markets can swing after policy announcements or election cycles.

Taxes and Compliance: Don’t Outsource Your Judgment

Residency, not passport, drives your taxes, and day‑count rules are only the start. Track presence by country, keep invoices and proof of economic ties, and maintain a tax buffer of 25–35% unless you’ve modeled your brackets. Use expat tax services for remote workers for filings, treaty claims, and social security coverage options, but learn the basics: permanent establishment risks, VAT on digital services, and withholding quirks. Align your budget buckets so each invoice auto‑allocates to tax, retirement, healthcare, and compliance costs.

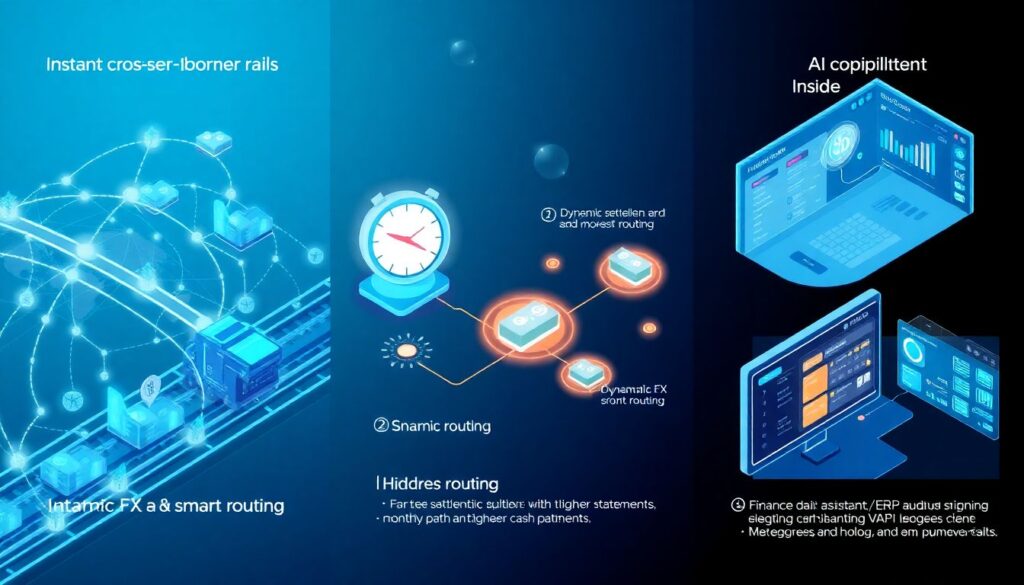

Trends to Watch in 2025

Three shifts matter now. First, instant cross‑border rails are expanding, shrinking settlement from days to minutes; cash flow planning can tighten. Second, card networks push dynamic FX and “smart routing”—great when transparent, costly when not; audit statements monthly. Third, AI copilots inside banks are improving dispute handling and merchant insights, but hallucinations still occur; verify critical outputs. Meanwhile, regulators ramp up travel rule compliance, so identity checks add friction—plan extra time when opening new accounts mid‑trip.

How to Choose: A Simple Decision Path

Start with your earning currency and top three spend countries. If most income lands in USD/EUR/GBP, prioritize multicurrency accounts with local details in those zones, then layer a lightweight budgeting app that syncs reliably offline. High‑mileage travelers should prefer cards with lounge day passes and robust insurance; occasional movers can focus on cash withdrawal limits. Re‑price your stack every quarter: compare FX spreads, card perks, and app fees. If the numbers don’t beat your base bank by 1–1.5%, switch without sentiment.

- Define a base currency for planning; convert all targets and reports to it.

- Maintain a 3–6 month runway split across two institutions and two countries.

- Automate invoice chasing and late‑fee rules for clients across time zones.

- Set FX alerts and pre‑fund big bills when rates hit your target band.

- Log country day counts and keep digital copies of key tax documents.

- Use best no foreign transaction fee credit cards for routine spend; pay in local currency to avoid DCC markups.

- Benchmark two remitters quarterly to secure the cheapest international money transfer for your corridors.

- Favor the best multi-currency accounts for digital nomads that offer fee‑free local rails for recurring bills.

- Test the best budgeting apps for digital nomads; keep one as the source of truth and export monthly.

- Schedule an annual check‑in with expat tax services for remote workers before major moves.