Set your shared money baseline

Start with a 60‑minute money date

Forget the stiff “budget meeting.” Brew coffee, open laptops, and pull up the last three months of statements. Your goal isn’t perfection; it’s clarity. Add up take‑home pay, list must‑pay bills, and average variable spending like groceries, fuel, and eating out. A couple I coached in Austin discovered they were each paying for streaming bundles, duplicating $58/month—$696 a year—just because no one had mapped it. Decide who owns which bill, agree on a personal “no‑questions” allowance (even $150 each reduces friction), and define what “we” are saving for in the next 12 months. Put work benefits on the table too: matches, HSA eligibility, and any RSUs. You’ll walk away with a picture that lets you make trade‑offs deliberately, not by accident.

Technical details: what to capture

– Net income: total after tax and deductions per pay period and per month.

– Fixed obligations: rent/mortgage, utilities, insurance, minimum debt payments.

– Variable averages: calculate 3‑month averages for groceries, dining, transit.

– Shared rules: spending threshold requiring a check‑in (e.g., $200).

– Target savings rate: start at 15% of net income; step up 1–2% every quarter.

Joint banking and friction‑free cash flow

Pick accounts that match how you live

Some couples thrive with one shared account; others prefer a “yours‑mine‑ours” setup: paychecks flow in, fixed bills and shared saving leave the joint account, and each partner keeps a small personal account for discretionary buys. If you search best joint checking accounts for couples, look for no monthly fees, early direct deposit, distinct debit cards with real‑time alerts, and automatic sweep rules to savings. One pair in Chicago set a rule: every Friday, any joint balance above $2,000 auto‑moves to savings, which added $4,800 in six months without willpower. Tie this to the best budgeting app for couples—think shared transaction tagging, category caps, and instant notifications—so you see the same numbers in one feed.

Technical details: automation that works

– Pay‑yourself‑first: route savings on payday, not month‑end.

– Buckets: separate high‑yield sub‑savings for “Emergency,” “Travel,” “Down payment.”

– Alerts: push notifications at 75% category spend to prevent end‑month scrambles.

– Overdraft armor: link savings as backup; avoid $30–$35 fees entirely.

Crush debt like a team, not roommates

Sequence matters more than sacrifice

List every debt: balance, APR, minimum, and whether it’s federal student, private, auto, or credit card. Pay minimums on all, then choose avalanche (highest APR first) for the fastest math win or snowball (smallest balance first) for the fastest emotional win. A couple I advised had two cards: $5,100 at 24.9% and $1,700 at 18.4%. By redirecting $300/month to the 24.9% card first, they saved roughly $680 in interest over 12 months versus snowballing. Refinance or consolidate only if the blended APR plus fees is at least 2–3 percentage points lower. And if your employer offers student loan match in lieu of 401(k) (a growing perk), capture it—it’s a guaranteed return you won’t get from extra lattes sacrificed.

Technical details: quick math checks

– Credit utilization: keep each card under 30% of limit; under 10% is ideal for scoring.

– Refi breakeven: refi if (old APR – new APR) × balance > fees within 18 months.

– Federal loans: know income‑driven plan options and forgiveness timelines before refinancing to private.

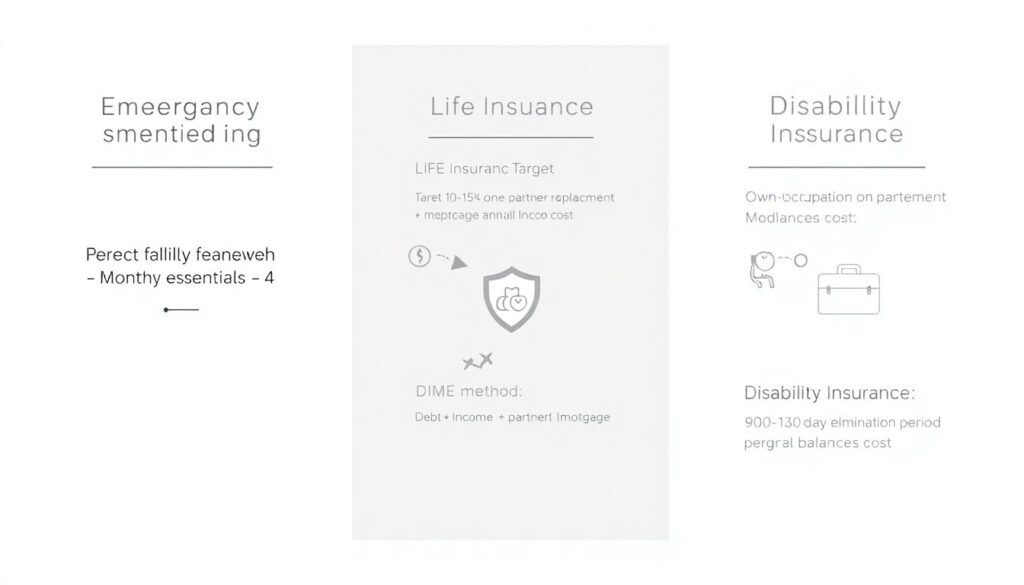

Build safety nets before chasing yield

Emergency cash and the right insurance

Aim for 3–6 months of essential expenses in a high‑yield savings account; two teachers I worked with targeted $18,000 and hit it in 14 months by auto‑saving $600 per paycheck. For insurance, prioritize disability (it protects your paycheck) and term life sized to actual needs. Healthy non‑smokers in their late 20s often see term life insurance quotes for young couples around $20–$35 per month per person for $500,000 of 20‑year coverage, depending on underwriting class. Skip pricey whole life until your investing and protection basics are set. Review employer benefits: sometimes the cheapest starter disability coverage is at work, and adding a private policy later can top off to 60–70% income replacement.

Technical details: sizing coverage

– Emergency fund: monthly essentials × 4 is a practical midpoint to start.

– Life insurance: target 10–15× one partner’s annual income, or DIME method (Debt + Income replacement + Mortgage + Education).

– Disability: own‑occupation if possible; 90‑ to 180‑day elimination period balances cost and protection.

Invest early, even while paying debt

Capture matches and keep it simple

The easiest win is the employer match—if your job matches 100% of the first 3% and 50% of the next 2%, that’s a 4% “raise” for contributing 5%. After capturing matches, consider Roth IRAs if you qualify; tax‑free growth and flexible basis withdrawals help with future goals. Keep portfolios boring: two or three low‑cost index funds (U.S. total market, international, and bonds). A newlywed duo in Seattle investing $500/month starting at 27 could reach roughly $500,000 by 57 at a 7% average return; wait 10 years to start, and you’d need ~1,020/month to hit the same mark. Automation beats willpower, and rebalancing annually keeps risk in check without you babysitting markets.

Technical details: allocation and costs

– Asset mix starting point: 100 minus your age in stocks as a joint average; adjust for job stability.

– Fund costs: aim expense ratios under 0.15%; fees compound against you.

– Tax order: 401(k) up to match → HSA (if eligible) → Roth/Traditional IRA → taxable brokerage.

Buying your first home without drama

Make the numbers pick the house

Before Zillow binges, run the math. Keep your total debt‑to‑income at or under 36% (up to ~43% can qualify, but comfort matters). First‑timers can put as little as 3–5% down on conventional loans and 3.5% with FHA if your score is 580+, but budget for PMI until you reach 20% equity. Compare first-time home buyer mortgage rates with at least three lenders and one credit union; even a 0.25% rate difference changes payments by roughly $15–$20 per month per $100,000 borrowed and can save thousands over the life of the loan. Consider buying points only if you’ll stay beyond the breakeven—roughly the cost of points divided by monthly savings. Don’t forget closing costs of 2–5% and a post‑close buffer for repairs.

Technical details: pre‑approval checklist

– Credit: pull all three bureaus; dispute errors early.

– Down payment: document source; large transfers trigger underwriter questions.

– Rate locks: typical 30–60 days; extensions cost money—time your search accordingly.

– Home fund: emergency fund stays separate; home maintenance set aside 1–2% of home value per year.

Make budgeting collaborative, not controlling

Tools and rituals that keep you aligned

Pick the best budgeting app for couples that supports shared categories, syncing across phones, and rules for recurring bills. Couples I see succeed run a 10‑minute weekly check‑in: glance at category progress, shift a little from “Dining” to “Gifts” if needed, and confirm the next transfer to travel or the down payment bucket. Use category caps, not judgment. If one of you travels for work, add a reimbursement category so those charges don’t blow up the month. And keep some joy money: $100–$250 each to spend guilt‑free preserves harmony while the plan hums along.

Technical details: fail‑safes

– Mid‑month reallocation: move dollars, not swipe the card blindly.

– Annual reset: bump savings goals by inflation + 1% to keep pace.

– Receipts: snap photos in app for shared visibility on big items.

When to bring in a pro

Know what you’re paying for—and why

If your situation includes equity comp, complex taxes, or conflicting money scripts, a fee‑only CFP can pay for themselves by preventing one big mistake. Searching financial advisor for newlyweds near me is a fine start, but screen for fiduciary duty, transparent pricing (flat fee or hourly for simple cases), and comfort answering “stupid” questions without jargon. For insurance, use an independent broker to compare carriers, then verify policy features directly. For mortgages, a broker can surface niche programs—physician loans, teacher grants, or state down payment assistance—that you won’t see on big aggregator sites, and they’ll help time locks versus first-time home buyer mortgage rates that move week to week.

Technical details: red flags and green lights

– Green: fiduciary, CFP designation, fee‑only, written scope of work.

– Red: commissions without disclosure, proprietary‑only products, vague performance promises.

– Reasonable fees: $200–$400/hour or $1,000–$3,000 flat for a comprehensive plan in straightforward cases.

Putting it all together in the first 90 days

Your sprint plan

Week 1: run the money date and set automation. Week 2: open or optimize joint banking, cancel duplicate subscriptions, and route savings to named buckets. Week 3: choose a debt strategy and request APR reductions; many card issuers will cut 2–4% if you’ve paid on time. Week 4: get term life insurance quotes for young couples and disability coverage, then enroll or adjust workplace benefits. Weeks 5–8: capture matches, set Roth contributions on autopilot, and implement your weekly 10‑minute budget ritual. Weeks 9–12: pull your credit reports, fix errors, and, if house‑curious, get pre‑approved so you can actually negotiate when the right place appears. Small moves, repeated, compound into a marriage‑strong money system.