Why a Debt‑Free Wedding Is the Smartest Gift You Can Give Yourselves

A “dream wedding” sounds exciting… until the credit card bills start showing up. Many couples quietly finance decor, dresses, and venues with loans—and then spend the first years of marriage paying for a one‑day event.

Going debt‑free doesn’t mean your wedding has to feel cheap or small. It means every choice is intentional. You’re buying memories, not monthly payments.

In this guide I’ll walk you step by step through how to save for a dream wedding without debt, сombining a conversational tone with a clear, analytical approach. You’ll see how to save money for a wedding fast when needed, how to plan a wedding on a budget without loans, and what actually works in real life—through concrete cases from couples who did it.

—

Step 1. Define What “Dream Wedding” Really Means (For You, Not Instagram)

Before you talk numbers, you need clarity. “Dream wedding” is vague—and vague dreams are expensive.

Clarify non‑negotiables

Sit down together and each write your top 3 priorities for the day, without looking at each other’s list. Examples:

– Great food

– Live music

– Intimate guest list

– Stunning photography

– Specific venue (e.g., family home, vineyard, city hall + restaurant)

Compare lists. Anything that appears on both is a non‑negotiable. Everything else is “nice to have.”

This simple exercise will drive almost every later decision and is one of the most underrated wedding budgeting tips to avoid debt.

Real‑life case: Anna & Mike’s “venue vs. everything else” choice

Anna dreamed of a historic mansion venue. Mike cared about great photos and a relaxed vibe. When they did the exercise:

– Both: photography, good food

– Only Anna: mansion venue

– Only Mike: live band

They requested quotes: the mansion alone would eat 55% of their total realistic budget. They realized: if they chose that venue, they’d have to cut photography and food or borrow.

They redefined the “dream”: a beautiful garden at a smaller event space, amazing photos, and a great dinner. Their guests remember the laughter and the pictures—not the building’s ceiling height.

—

Step 2. Set a Realistic Budget Using Backwards Planning

Instead of guessing what a wedding “should” cost, start with what you can actually save without pain.

Calculate your safe saving capacity

1. Add both take‑home monthly incomes.

2. Subtract non‑negotiable expenses (rent, groceries, minimum debt payments, transport).

3. Subtract reasonable lifestyle costs (not bare survival—realistic living).

4. What’s left is your maximum potential savings per month.

Now cut that number by 10–20%. That buffer protects you from surprise costs and prevents resentment (“we gave up everything for this wedding”).

Multiply the adjusted monthly savings by the number of months until your target wedding date. That total is your working budget ceiling.

Case: Short timeline vs. budget reality

Luis and Emma wanted to get married in 10 months. Together they took home $4,000/month. After expenses, they could save $900 comfortably. With a 15% buffer, they targeted $765/month for wedding savings.

– $765 × 10 months = $7,650 total budget

They’d initially imagined a $20,000 wedding because “that’s what our friends paid.” Seeing the math, they had three logical choices:

– Reduce the wedding scope

– Extend the timeline

– Increase income (side jobs)

They chose to extend to 16 months and each picked up one small weekend gig. End result: ~ $14,000 budget, no loans, no panic.

This backwards‑planning method is the backbone of the best wedding savings plan for couples: start from the real money you can save, not from social expectations.

—

Step 3. Build a Simple, No‑Nonsense Wedding Savings Plan

You now know how much you can save per month and your target total. Time to systematize it.

Create a dedicated “wedding fund” (not just mental math)

Open a separate high‑yield savings account titled “Wedding Fund.” Automate transfers the day after paychecks land. If the money never hits your everyday account, you’ll be far less tempted to spend it.

What works well for many couples:

1. Fixed monthly transfer (your base amount).

2. Optional “top‑ups” from bonuses, tax refunds, or extra income.

3. A rule: no withdrawals except for pre‑planned wedding expenses.

Micro‑goal breakdown

Large goals feel abstract. Split your wedding budget into smaller, dated milestones:

– Month 3: $2,000 saved

– Month 6: $4,500 saved

– Month 9: $7,000 saved

Check in monthly. If you’re behind, adjust: either trim some wedding costs or temporarily increase income. This keeps you in control instead of drifting towards last‑minute borrowing.

—

Step 4. Prioritize Spending: What Deserves the Money (and What Doesn’t)

When people ask how to plan a wedding on a budget without loans, the honest answer is: you can’t have everything at full price. You must choose.

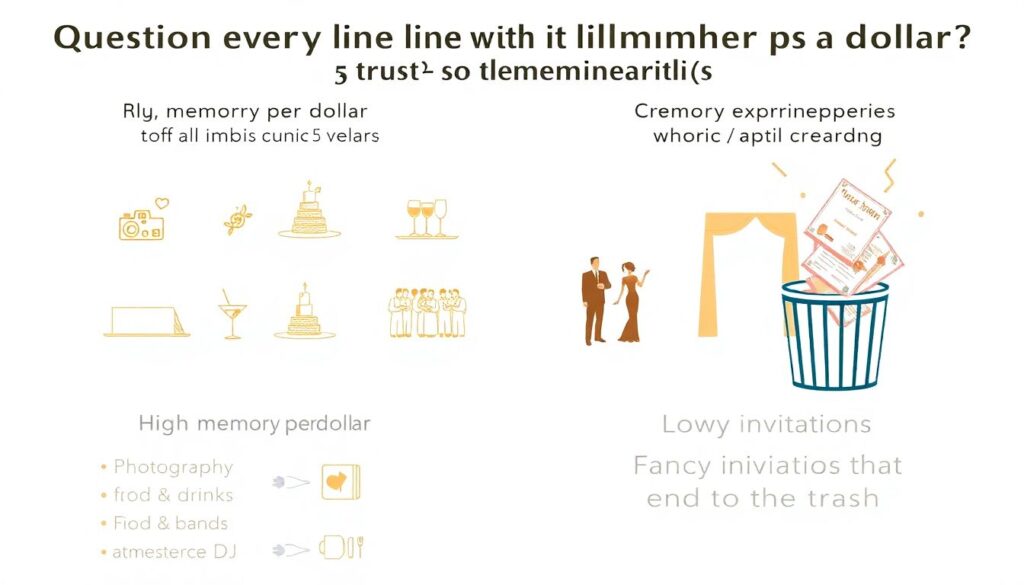

Use the “memory per dollar” filter

Question every line item with: “Will we or our guests remember this in 5 years?”

High “memory per dollar” items often include:

– Photography / videography

– Food and drinks

– Ceremony experience

– Music / atmosphere

Low “memory per dollar” items frequently are:

– Fancy invitations that end up in the trash

– Overly elaborate favors nobody uses

– Expensive chair covers, napkin rings, or specialty cutlery

– Second (or third) outfit changes

Case: Ditching favors, upgrading food

Nora and James initially budgeted:

– $600 for personalized wedding favors

– $1,000 for basic buffet catering

They asked themselves: Will anyone remember a tiny bottle of olive oil with our initials on it? Probably not. But they will remember the food.

They dropped favors completely and moved that $600 into catering. For an extra $600, they upgraded to family‑style platters and one signature cocktail. Guests raved about the dinner. Nobody asked about favors.

That’s how to save for a dream wedding without debt: pay for things that impact experience, quietly eliminate the rest.

—

Step 5. Learn How to Save Money for a Wedding Fast (Without Burning Out)

Sometimes the date is closer than your savings number. You need acceleration, but not chaos.

Use the “temporary intensity” rule

Intense cost‑cutting works for short bursts, not as a lifestyle. Decide on a defined sprint, e.g., “For 3 months we’ll…”:

– Limit eating out to once a week

– Pause non‑essential subscriptions

– Cap clothing/beauty spending

– Sell unused items (electronics, designer pieces)

Put 100% of these extra funds straight into the wedding account.

Case: Three‑month sprint that added $3,100

Priya and Daniel were $3,000 short with 5 months left. Instead of taking a small loan, they did a 3‑month sprint:

– Sold an unused bike, camera, and old phone: $1,100

– Cut restaurants from $350/month to $120/month: saved $690 in 3 months

– Paused two streaming services and a gym membership (used home workouts instead): saved $210

– Took two extra freelance projects: $1,100 after tax

Total: $3,100 in 3 months. Was it fun? Not always. Was it worth starting married life without extra debt? Absolutely.

This is a practical answer to how to save money for a wedding fast while still keeping your sanity: short, focused sacrifices with clear end dates.

—

Step 6. Use “Cheap Wedding Ideas to Save Money” That Don’t Look Cheap

Cutting costs doesn’t have to mean cutting beauty or joy. The trick is choosing frugal ideas that don’t feel like compromises.

Venue & timing hacks

– Off‑peak days: Thursday or Sunday weddings, or Friday evenings, can be 20–40% cheaper than Saturday prime time.

– Shoulder seasons: Late fall or early spring often mean lower venue and vendor rates.

– Single location: Ceremony and reception in one place reduces transport, decor duplication, and rental fees.

Case: Sunday brunch wedding win

Leo and Marissa loved a specific restaurant but the Saturday evening minimum was $12,000—way over budget. The manager mentioned a Sunday brunch option:

– Food cost down by ~35%

– Alcohol spend lower (daytime vs late‑night drinking)

– Venue fee reduced because it was normally closed then

Total savings: about $5,000. Guests loved the relaxed vibe, daylight photos were incredible, and they avoided late‑night drama entirely.

Decor shortcuts that still look intentional

– Focus decor where guests spend the most time (entrance, reception tables, photo spot).

– Use candles and greenery instead of elaborate floral arrangements on every surface.

– Borrow decor from recently married friends (vases, candle holders, signs).

A lot of the best cheap wedding ideas to save money are about subtraction, not addition: fewer elements, larger impact.

—

Step 7. Avoid the Most Common Money Mistakes Couples Regret

Certain patterns show up again and again in couples who overspend.

Mistake 1: “We’ll just put overruns on a card and figure it out later”

This is how small overruns snowball into multi‑year payments. The emotional high of wedding planning makes future debt feel abstract.

Better approach: build a 5–10% “unknowns” category into your budget from the start. If that fills up, you don’t borrow—you cut or swap something.

Mistake 2: Expanding the guest list without updating the budget

Each added guest increases:

– Food and drink

– Chair/table rentals

– Favors (if any)

– Invitation costs

– Sometimes venue size

Yet people often add 10–30 guests “because we feel bad not inviting them” without recalculating. Before saying yes to additional guests, recalculate per‑person cost and decide if it still fits your priorities.

Mistake 3: Asking parents for help without clear boundaries

Family contributions can be a blessing—or a source of pressure. If parents insist on inviting more people because “we’re paying,” costs can balloon.

Clarify early:

– Are they giving a fixed amount (e.g., $3,000) or paying for specific items (e.g., dress, bar)?

– Does their contribution give them decision rights over the guest list or vendors?

This prevents emotional debt from replacing financial debt.

Case: Guest list creep that almost caused a loan

Mila and Ryan originally planned 80 guests. Their per‑person cost (food + rentals + service) was about $95.

Then came:

– “Your cousins should come.” (+10)

– “We have to invite all the coworkers.” (+12)

– “What about the neighbors?” (+6)

New total: 108 guests. Additional cost: about $2,660.

They’d already maxed their budget. The venue suggested, “Many couples just put the difference on a card.” Instead, they did the math out loud with their families. Hearing “Those extra 28 guests will cost about $2,600” reframed the conversation. They compromised: some distant contacts were invited to a casual post‑wedding BBQ instead of the main reception.

No loan needed.

—

Step 8. Negotiate Like Adults, Not Like Embarrassed Customers

Negotiation isn’t rude; it’s normal business. Done respectfully, it can save hundreds or thousands.

How to negotiate without being “that client”

1. Do basic research first. Know average local prices so your expectations are reasonable.

2. Be transparent about your budget. “We love your work. We’re trying to keep photography under $1,800. Is there any smaller package or weekday option?”

3. Trade scope, not value. Instead of demanding discounts, reduce hours, number of edited photos, or add flexibility on timing.

4. Ask about off‑peak deals. Vendors often have quieter days they’re happy to fill at lower rates.

Case: Photographer compromise that saved $700

Sara and Jonah wanted a specific photographer whose standard full‑day package was $2,500. Their budget: $1,800 max.

They emailed honestly:

– They loved her work.

– They couldn’t stretch to the full package.

– They would be happy with fewer hours and only digital files, no album.

The photographer offered:

– 6 hours of coverage instead of 10

– Digital delivery only

– Weekday rate

Price: $1,800. Everyone was satisfied.

This is how to plan a wedding on a budget without loans: you adjust length and extras, not your principles.

—

Step 9. Align With Each Other So Money Doesn’t Become the Real Fight

The wedding is just one day. Your money habits as a couple will last decades. Use planning as practice for how you handle finances together.

Set decision rules together

Agree in advance:

– Any expense over $X must be discussed (e.g., $300).

– No “secret upgrades” as a surprise to the other person.

– A monthly budget check‑in where you review spending and remaining savings goals.

Case: Avoiding the “dress vs. DJ” resentment

Chloe secretly spent $1,800 on a dress they’d budgeted $1,000 for, thinking, “I’ll just find a way to make it up later.” When they later needed to cut something, her partner suggested reducing DJ hours. It turned into a fight about fairness.

They eventually sat down, created a “no solo big purchases” rule, and decided future upgrades would only happen if they both agreed where the extra money was coming from (additional savings, cutting something else, or extra work). The process improved their communication far more than the exact numbers.

A calm, transparent approach to money is worth more than any decor piece.

—

Step 10. Final Checklist: Your Debt‑Free Wedding Game Plan

To bring everything together, walk through these actions in order:

1. Define priorities. Each list your top 3; agree on shared non‑negotiables.

2. Calculate safe savings. Work backwards from your monthly capacity and timeline to set a realistic budget.

3. Open a wedding fund. Automate contributions and track milestone goals.

4. Allocate by “memory per dollar.” Invest in what truly matters; strip out low‑impact extras.

5. Plan a saving sprint if needed. Use a 2–3 month period for intensified savings or extra income.

6. Leverage smart, cheap wedding ideas to save money. Off‑peak dates, simpler decor, and single‑location events.

7. Add a 5–10% buffer. Avoid “just put it on a card” thinking.

8. Negotiate respectfully. Adjust scope instead of taking loans.

9. Review together monthly. Prevent surprises and resentments.

When you follow these steps, you’re not just learning how to save money for a wedding fast or cutting costs randomly. You’re designing a wedding that matches your values and building financial habits that support your future together.

The real “dream” isn’t just the perfect photos; it’s waking up after the honeymoon and realizing you own every memory of that day outright—no lender, no looming balance, just the two of you and a clean financial slate.