When the numbers on the screen start to look scarier than a horror movie, “budgeting” stops being a nice-to-have skill and turns into a survival tool. A difficult financial year can feel like a wave you’re not ready to surf. But with a clear resilience plan, that wave becomes something you can ride — not something that drags you under.

Below — a practical, motivating walkthrough of budgeting for a difficult financial year: a resilience plan, with real stats from 2022–2024, inspiring stories, and concrete tools you can start using today.

—

Why a “resilience plan” matters more in 2025 than ever

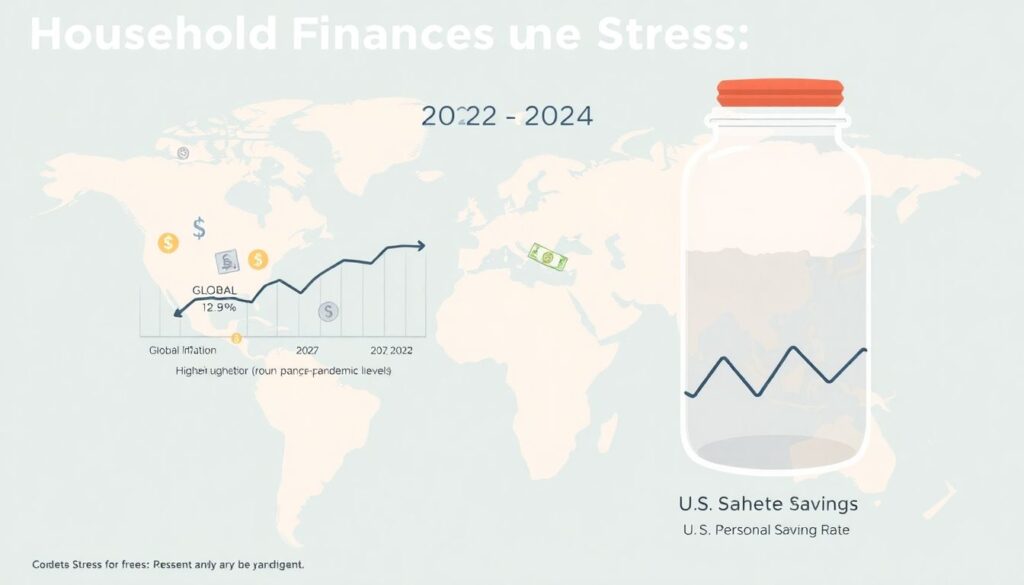

The last three years have been a stress-test for household finances worldwide. Between 2022 and 2024:

– Global inflation peaked around 8–9% in 2022 and then cooled, but still stayed above pre‑pandemic levels in many countries through 2023–2024 (IMF estimates).

– In the U.S., the personal saving rate fell from double digits in 2020 to roughly 3–6% during 2022–2024, hovering near historical lows.

– Central banks raised interest rates sharply, which made mortgages, credit card balances and personal loans noticeably more expensive by late 2023 and 2024.

In other words: prices jumped, borrowing got pricier, and savings cushions got thinner. That’s exactly the kind of backdrop people have in mind when they google budgeting for recession 2025 — and it’s not paranoia; it’s smart preparation.

A resilience plan is simply a budget built for turbulence: it expects shocks, it absorbs them, and it helps you recover faster.

—

Step one: Face the numbers (without panicking)

Let’s start with the hardest move: opening all the tabs and looking at everything.

In 2024, several surveys in the US and Europe showed that 40–60% of people admitted they “avoid looking at” their full financial picture because it stresses them out. Ironically, this avoidance is what turns a manageable problem into a crisis.

If you’re wondering how to create a personal budget in a financial crisis, here’s the simplest, low-stress starter:

– List *all* income sources (after tax): salary, side gigs, benefits, child support, rental income.

– Pull the *last 3 months* of transactions from bank and card statements.

– Highlight essentials: rent/mortgage, utilities, groceries, transport, medications, childcare.

– Mark everything else as flexible or optional.

You’re not judging yourself here; you’re just collecting data like a scientist. Think of this as doing a financial MRI: it can feel uncomfortable, but you can’t treat what you refuse to see.

—

Turning a messy year into a simple, living budget

A difficult financial year doesn’t need a complicated spreadsheet from day one. It needs a simple, repeatable system that survives stress.

A lot of resilience budgets use a modified 50/30/20 rule. In a crisis, it might look more like:

– 60–70% essentials

– 10–15% “breathing room” (small joys, irregular costs)

– 15–30% debt payments, savings, and emergency buffer

Even if your numbers are way off these ranges right now, they give you a direction — not a verdict. The point is to push, month by month, toward a share of your income that builds safety instead of just surviving.

Short version: your budget is not a punishment list. It’s a map that says, “Given THIS reality, how do I get the most control and calm possible?”

—

Inspiring examples: People who built resilience in rough years

Let’s bring it down to human scale.

Case 1. Maria, marketing manager, 2022–2024

– 2022: Maria’s rent in Madrid jumps 14% while food prices climb. Her savings rate drops from 12% to 3%.

– 2023: She decides to treat her finances like a project at work. She exports 12 months of transactions, tags spending categories using an app, and discovers that food delivery and “small online shopping” eat almost 18% of her take‑home pay.

– Action: She sets a cap: only two deliveries a month, and every “non-essential” online purchase has to wait 24 hours.

– 2024 result: She pays off a high‑interest credit card completely and gets her savings back up to 10% of income — still lower than before, but she’s out of “red alert” mode.

Case 2. Jamal, electrician turned side‑hustle entrepreneur

When overtime hours dried up in 2023, Jamal’s income dipped 20%. Instead of waiting for things to go back to “normal,” he broke his resilience plan into three small moves:

1. Cut streaming and subscriptions except one shared account.

2. Turned a casual weekend repair habit into a small paid side gig.

3. Used a 0% balance transfer offer as part of a debt consolidation and budgeting plan, so he could pay down his most toxic debt without extra interest.

By the end of 2024, he wasn’t rich. But he had fewer debts, more predictable payments, and a small emergency fund. That’s resilience in action: not glamorous, but powerful.

—

How to engineer a “crisis-proof” monthly routine

Once you’ve mapped your income and spending, you need habits — the auto‑pilot that keeps your plan alive when you’re tired, stressed, or overloaded.

Here’s a simple monthly rhythm that works well in a difficult financial year:

– Before payday: Check what bills are coming, note any irregular expenses (birthdays, car service, school fees).

– Payday + 1 day: Automatic transfers — debt, savings, and essentials first.

– Mid‑month check‑in: 10–15 minutes to see whether you’re on track for groceries, transport, and “small pleasures.”

– End‑of‑month review: What surprised you? What do you want to adjust next month?

In 2022–2024, people who used at least one digital tool to track their finances (bank app categories, spreadsheets, or a dedicated budgeting app) reported higher savings rates and lower stress in multiple consumer surveys. The routine matters more than the tool, but the right tool can make the routine painless.

—

Tools that actually help: Apps, not anxiety

If your budget lives only in your head, it will lose to emotions almost every time. That’s where apps are practical, not trendy.

Many of the best budgeting apps for saving money fast share three things:

– Real-time syncing with your bank accounts and cards

– Clear category limits (for example, caps on eating out or transport)

– Simple visuals: how much you’ve spent and what’s left this month

You don’t need a perfect app; you need one you’ll actually open. For some people that’s a minimalist tracker. Others prefer a more “all-in-one” tool that connects to financial planning services for economic downturn, offering advice, alerts, and even access to human planners.

If apps are not your thing, a shared spreadsheet with color‑coded categories achieves the same logic, just with a bit more manual work.

—

Smart cuts versus self‑sabotage

When income drops or prices jump, the instinct is to cut everything. But a resilience plan is about smart trade‑offs, not self‑punishment.

Typical smart cuts:

– Duplicate subscriptions (you probably don’t need four platforms).

– “Convenience” fees: constant delivery, impulse snacks, premium shipping.

– Underused services: gym you don’t visit, apps you forgot you pay for.

Dangerous cuts:

– Medicines and health check‑ups

– Key tools that protect income (transport, basic internet, work equipment)

– So‑called “tiny joys” if they are your mental health pressure valve

Many people who went too harsh in 2022—e.g., cutting all social life and treats—reported burnout and then bounced back into overspending. Sustainable budgeting respects the human you, not just the numbers.

—

Case studies: Successful resilience projects, not just lucky breaks

Think of your money like a project with phases, deadlines, and outcomes. Here are a few short, real‑world inspired “projects” from the last three years.

Project A: The 90‑day reset (couple, joint budget)

– 2022: Two teachers in the UK end the year with a growing overdraft and no idea where the money goes.

– Step 1: For 30 days, they track every expense without changing habits.

– Step 2: For the next 60 days, they apply three rules: cash envelopes for groceries, spending cap for weekends, no‑questions‑asked personal pocket money for each.

– Result by mid‑2023: Overdraft gone, small emergency fund started, arguments about money drop sharply.

Project B: Freelance income roller coaster, stabilized (solo worker)

– 2023: A freelancer’s income swings wildly month to month. In 2022 he saved nothing and relied on credit cards in slow months.

– Action: He sets a “fake salary”: each month, he transfers only a fixed amount from his business account to his personal account and leaves the rest as a shock absorber.

– By late 2024: Even though annual income didn’t grow much, his stress dropped dramatically. He created a personal safety net by smoothing the ups and downs.

The common theme: they didn’t wait for conditions to improve. They treated resilience as a project with clear, bite‑sized steps.

—

Skill-building: Upgrading yourself as part of the budget

A powerful twist in a resilience plan is seeing learning as a budget line, not an afterthought. You don’t just cut; you also invest in your future earning power.

Focus on three types of development:

– Income stability: Skills that make you harder to replace (automation tools, customer management, data basics, advanced Excel).

– Income expansion: Skills that can turn into side income (language tutoring, digital design, coding, copywriting, trades).

– Financial literacy: Understanding interest, risk, taxes, and investing basics.

Between 2022 and 2024, online learning platforms reported sustained growth in enrollment for finance and career skills, especially during periods of bad economic news. People weren’t just reacting; they were quietly upgrading.

You don’t need expensive courses to start. Many high‑quality resources are free or low‑cost.

—

Learning resources: Where to train your financial resilience

Here are some types of resources that can help you strengthen both your budgeting skills and your earning potential:

– Free courses on personal finance and investing from universities (MOOCs on major platforms).

– Budgeting and money podcasts that break down real‑life cases, not just theory.

– Community or nonprofit workshops that offer one‑on‑one counseling or financial planning services for economic downturn, often with no or low fees.

– Local libraries that give you access to books, online databases, sometimes even financial education events.

When you choose a resource, look for three signs: evidence‑based content (not just opinions), transparency about risks, and no pressure to buy specific financial products.

—

Handling debt: From “black hole” to structured plan

Debt becomes especially scary in a difficult year because rising interest rates make past decisions more expensive. But hiding from debt doesn’t work; organizing it does.

If your debts feel overwhelming, consider turning them into a single, clear roadmap:

– List all debts: balance, interest rate, minimum payment.

– Prioritize either highest interest (debt avalanche) or smallest balance (debt snowball).

– Decide how much above the total minimum you can put toward debt each month.

In some cases, a structured debt consolidation and budgeting plan can help: combining multiple debts into one payment at a lower overall rate. But this only works if you also fix the habits that created the debt; consolidation is a tool, not magic.

From 2022–2024, regulators repeatedly warned about aggressive lenders and “too good to be true” consolidation offers. Reading the fine print and getting neutral advice before signing anything is part of modern financial resilience.

—

Emergency funds, even when money is tight

You’ve probably heard the classic rule: 3–6 months of expenses saved. For many people in 2022–2024, that sounded about as realistic as buying an island.

So reframe it.

Instead of chasing a giant number, build resilience in layers:

– Layer 1: 100–200 units of your local currency (enough for groceries or a small emergency).

– Layer 2: One full month of essential expenses.

– Layer 3: Three months, built slowly, over years, not weeks.

What the data shows: households with *any* emergency savings — even a few hundred dollars/euros — were significantly less likely to rely on high‑interest credit after sudden shocks in 2022–2023. Tiny buffers still change outcomes.

Your budget’s job is to carve out even 1–5% of income to start this buffer. Tiny, boring transfers that quietly change your future.

—

Bringing it all together: Your personal resilience blueprint

Let’s connect the dots into a simple, customizable plan you can adapt today:

– Accept reality without drama: prices rose, rates rose, savings fell.

– Map your current situation honestly.

– Build a simple, flexible monthly budget with clear priorities.

– Use tools — apps or spreadsheets — to keep yourself honest.

– Protect key areas (health, income tools, mental health) while cutting the rest strategically.

– Upgrade your skills and knowledge to improve both earnings and decisions.

– Tackle debt with a structured, realistic approach.

– Grow an emergency fund in layers, not in one heroic leap.

If the idea of budgeting for recession 2025 makes you nervous, remember: a resilience plan isn’t about predicting the future perfectly. It’s about making sure that, whatever comes next, you’re a little less fragile and a lot more prepared than you were last year.

You don’t need a perfect year to start. You just need one decision today: “I’m going to treat my money like something I can design, not something that just happens to me.” From there, every small, consistent step becomes part of your resilience story.