Why pocket money needs a purpose now, not “later”

Handing kids a few dollars “just because” used to feel harmless. Today, with tap‑to‑pay everywhere and money turning invisible, that approach quietly backfires.

Over the last three years, several trends converged:

– According to Greenlight’s 2023 report, teens using their app spent 23% more online compared to 2021.

– T. Rowe Price’s 2023 “Parents, Kids & Money” survey found that 47% of parents still avoid talking about money with their kids because it feels “too stressful” or “too early”.

– Yet GoHenry’s 2022 youth finance report showed that kids who regularly receive an allowance and manage it digitally save 2–3x more than those who don’t.

The gap is obvious: kids are spending in a digital world, while many parents are still teaching money like it’s 1995.

A purposeful kids allowance system closes that gap. It turns pocket money from a weekly ritual into a low‑risk, high‑impact simulator of real life — with you as the coach, not the bailout machine.

—

From pocket money to “practice economy”

The idea is simple: treat pocket money as a small, controlled “economy” where children can make real choices, face real consequences, and learn real financial skills — while the stakes are still tiny.

What makes an allowance “purpose‑driven”?

Not the amount. Not the fancy app. The *design*.

An effective, intentional system usually has four ingredients:

– Clear structure – when, how much, and under what conditions allowance is given.

– Visible trade‑offs – kids must choose between saving, spending, giving, and maybe investing.

– Real‑time feedback – they see numbers change when they act.

– Reflection – you talk, briefly and regularly, about what worked and what didn’t.

Notice what’s *not* on the list: perfection, spreadsheets, or giving a lecture every time they buy candy.

—

Inspiring examples: what it looks like in real families

Example 1: The “family finance board” (ages 6–9)

A family in Canada created a simple Sunday ritual:

– Each child gets a small fixed allowance, split automatically into three jars (Save / Spend / Share).

– Once a month, they review the jars and set one tiny goal for the next month: “Buy a comic”, “Donate to the animal shelter”, “Save for a Lego set”.

– Parents ask one question only: “What did you notice about money this month?”

After a year, their 8‑year‑old started negotiating with himself: “If I wait two more weeks, I can buy the bigger set.” That’s delayed gratification in action — the kind that famous marshmallow experiments connect with better long‑term outcomes.

Example 2: The “pre‑salary” model (ages 10–13)

A single mom in the UK was tired of random requests: bus money, snacks, birthday gifts.

She re‑framed it:

– Her son gets a fixed “monthly salary” that’s meant to cover specific categories: school snacks, games, small gifts for friends.

– Together they made a very simple budget. When it’s gone, it’s gone.

– At the end of the month, they review: Which categories went over? Where did he surprise himself?

Within six months, he’d started building a buffer. Not because his mom lectured him, but because it *felt* bad to be broke in week three. That emotional lesson sticks far better than any worksheet.

—

Why digital tools changed the allowance game

Cash is great for young kids, but it has two big problems today:

1. Kids see you tapping a card or phone; cash feels like a different universe.

2. Most of their “real” spending (games, subscriptions, online shopping) is digital.

That’s why a new wave of tools — from a simple debit card for kids with allowance to a chore and allowance tracking app — has exploded in the last three years. They give kids a sandboxed version of digital money.

What the data shows about digital pocket money

Between 2021 and 2023:

– Greenlight (a popular US app) reported that teens using their platform grew their average savings balance by 40%.

– GoHenry’s European data showed that kids actively using money management tools for children checked their balances 5–10x more often than kids relying on cash alone.

– Several providers reported that around 70–80% of parents used transaction notifications as conversation starters about spending choices.

Is every app perfect? Of course not. But the pattern is clear: when kids see their money move on a screen — like adults do — financial concepts become less abstract and more “real”.

—

How to design a kids allowance system that actually teaches something

You don’t need a PhD in finance to build a system that works. You need a plan and some consistency.

Step 1: Decide the “why” before the “how much”

Ask yourself:

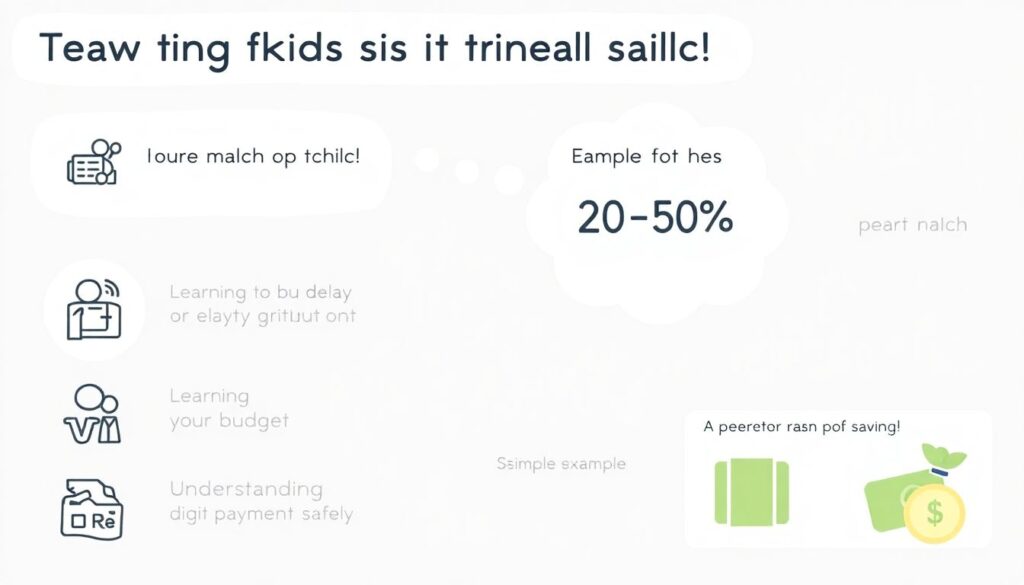

– Do I want my child to learn to delay gratification?

– To budget?

– To give?

– To understand digital payments safely?

Pick your top two priorities. The rest is optional.

Then decide your rules *around* those priorities. For example:

– If the priority is saving, you might match 20–50% of whatever they put into savings.

– If it’s budgeting, you might give slightly more — but make them cover more categories themselves.

– If it’s digital literacy, you might move early to a supervised card or app.

Step 2: Pick your tools (low‑tech or high‑tech)

You can stay fully analog — jars, envelopes, notebooks — and still teach powerful lessons. Or you can look at the best allowance apps for kids and choose one that fits your values and your kid’s age.

When you evaluate an app or card, look for:

– Separate pots or “buckets” (Spend / Save / Give)

– Goal‑setting features your child can see and adjust

– Clear parental controls and real‑time alerts

– Age‑appropriate visuals: not too childish for teens, not too complex for younger kids

Digital isn’t automatically “better”, but it’s often more aligned with the way money works in your child’s actual world.

—

Chores, work, and the “money myth”

A huge debate in parenting circles:

“Should kids get allowance for chores?”

Here’s a practical, research‑aligned middle path.

Separate “family duties” from “paid work”

Studies in the early 2020s (including work highlighted by the American Psychological Association) show that tying *all* chores to money can weaken the sense of contribution and intrinsic motivation.

A balanced model many families have used successfully:

– Non‑negotiable chores (cleaning room, dishes, helping with meals) = part of being in the family, no pay.

– Extra tasks (washing the car, deep cleaning, yard work) = optional, paid “jobs”.

A chore and allowance tracking app can help here, not as a surveillance tool, but as a shared dashboard. Kids see what’s expected no matter what; they also see “extra gigs” they can pick up to earn more.

This teaches two parallel truths:

1. “I contribute because I belong.”

2. “If I want more money, I can increase my effort and value.”

Both are essential for healthy adult money habits.

—

Real cases: what’s working in successful projects

Case 1: School‑based allowance lab

In 2022–2023, a pilot “money lab” in several European schools (reported in GoHenry’s youth finance initiatives) let students manage a small, simulated monthly budget through a child‑friendly app.

– Students allocated funds to virtual categories: lunches, outings, “emergency”, donations.

– They had to deal with surprise “events”: lost bus card, broken headphones, class trip.

– Teachers facilitated short debriefs: “Who ran out early? What would you change next month?”

After one school year:

– Over 75% of students said they felt “more confident” about handling money.

– Teachers reported fewer “impulse buy” fundraisers and more kids asking upfront about cost and value.

The big insight: you don’t need huge amounts. You need repetition and reflection.

Case 2: Family using a hybrid digital‑cash model

A US family with two kids (9 and 12) shared their three‑year journey in a 2023 parenting finance forum:

– Weekly base allowance goes onto a kids’ debit card, divided into Spend/Save/Give.

– Small cash amounts are still used for very local things (lemonade stand, neighbors’ garage sales).

– Every quarter, they do a “money review evening”: kids show their spending categories, parents show a simplified version of their own budget.

Results after three years:

– Both kids keep at least one month of “buffer money” on their cards.

– The 12‑year‑old started a small online design gig and automatically moves 20% of income to long‑term savings.

– Money talks at home are shorter, calmer, and more fact‑based because everyone can *see* the numbers.

This is a living, breathing money education — not a one‑time lecture.

—

Practical recommendations by age

Ages 5–8: Make money visible and concrete

Goals:

– Understand that money is limited

– Start distinguishing between “now” and “later”

– Connect small work with small rewards (without over‑monetizing everything)

Try:

– Clear jars or transparent envelopes for Spend / Save / Share

– Short, visual goals (“When this jar hits here, we buy the puzzle”)

– Very simple language: “We can’t buy everything, so we choose.”

Limit digital tools here to *you* tracking; they don’t need an app yet.

—

Ages 9–12: Bridge to digital and simple budgeting

Goals:

– Plan for a month, not a day

– Take responsibility for some categories (snacks, small gifts)

– Learn from small mistakes with minimal rescuing

Try:

– A basic kids allowance system with fixed paydays and simple rules

– Introducing a supervised card or app once they show consistency

– Letting them overspend once in a while — and experience waiting until the next “payday”

This is a good stage to introduce a debit card for kids with allowance, as long as alerts and limits are in place and you keep talking about choices, not just amounts.

—

Ages 13–17: Simulate adult money

Goals:

– Manage recurring expenses

– Balance short‑term fun vs. long‑term goals

– Understand digital risks (fraud, subscriptions, social pressure)

Try:

– Monthly allowance that covers several categories (transport, phone share, entertainment)

– Joint review of their app or bank data: “What patterns do you see?”

– Linking part of their money to earnings from real work (tutoring, part‑time job, online projects)

At this age, money management tools for children should look and feel close to adult tools — not cartoonish — but still give you parental controls, spending limits, and education prompts.

—

Common mistakes that quietly undermine learning

You can have the coolest setup and still sabotage the lessons if you’re not careful.

1. Rescuing every shortfall

If you always top up when they run out, your child is learning: “If I overspend, someone will fix it.”

A better script:

“I see this is frustrating. Let’s think about how to avoid this next month. What could you change?”

2. Changing the rules every time you feel guilty

Consistency beats complexity. If you want to adjust the system, do it on a future date, not in reaction to a meltdown at the checkout.

3. Treating the app as a babysitter

Technology is a tool, not a teacher. The real learning happens in short, honest conversations about why they made a choice and how they feel about it now.

—

Resources to go deeper (without drowning in information)

You don’t need a full curriculum. You just need a few solid, practical inputs.

Learning for parents

– Books & guides

– “The Opposite of Spoiled” by Ron Lieber – thoughtful approach to money and values.

– “Make Your Kid A Money Genius (Even If You’re Not)” by Beth Kobliner – age‑by‑age scripts.

– Organizations & reports

– OECD and OECD PISA financial literacy reports (2021–2023) for big‑picture context.

– National financial literacy initiatives in your country (many updated their youth sections post‑2021).

Learning with kids

– Short, story‑based videos on how bank cards, interest, and online payments work.

– App‑based “challenges” some platforms now include: save for a goal, track spending for a week, donate to a cause.

– Family money meetings: 15–20 minutes once a month to review goals, not problems.

Use the best allowance apps for kids as teaching aids, not just payment methods: walk through transaction histories together, talk about scams, check progress toward goals.

—

Bringing it all together: pocket money as practice for real life

Your child will eventually:

– Get paid for their work

– Choose between short‑term pleasure and long‑term security

– Handle digital payments, subscriptions, and maybe debt

You can let all of that happen “for the first time” at 18 — or you can let them rehearse now, with $5 and your guidance.

A purposeful allowance system doesn’t promise a future millionaire. It does something far more realistic and powerful:

– It gives your child a safe arena to make mistakes.

– It anchors money in values, not just numbers.

– It builds quiet confidence that “I can handle this.”

Start small. Pick one change: a clearer rule, a simple app, a monthly review, separate jars. Run it for three months, then adjust.

Money will be part of your child’s life whether you talk about it or not. Turning pocket money into practice is your chance to make that relationship healthier, calmer, and far more capable.