Why Micro‑Saving Beats Massive Sacrifice

Recent numbers: why small wins matter

If it feels harder to save than it used to, you’re not imagining things. According to Federal Reserve data, the U.S. personal saving rate, which spiked above 15% during pandemic stimulus in 2020–2021, slid down to roughly 3–5% through 2022–2023, hovering near its lowest levels in over a decade. Eurostat reports a similar pattern in many EU countries: an elevated saving rate in 2020 followed by a steady decline as inflation and housing costs rose through 2021–2023. In parallel, surveys from organizations like Bankrate and the CFPB show that around 35–40% of households had difficulty covering a $400–$500 emergency in those same years. I don’t have data for 2025–2026 yet, but the trend up to 2023 is clear: traditional money saving tips that rely on big leftover chunks of cash simply don’t match current cost‑of‑living pressure.

Micro‑saving takes a different angle: instead of asking “how do I save hundreds every month?” it asks “how do I trap $1–$5 at a time, dozens of times a week, without feeling it?” Behavioural finance research over the last three years keeps confirming a predictable pattern: people stick with small, low‑friction behaviours far more consistently than with radical lifestyle overhauls. Product data from major fintechs between 2021 and 2023 shows that “round‑up” features, automated micro‑transfers and cash‑back sweeps consistently increase the number of days per month a user actually saves, even if each action is tiny. When you string those tiny actions together, they become one of the most effective ways to save money each month without triggering the usual willpower battles.

Necessary Tools for Everyday Micro‑Saving

Digital toolkit: apps and automation you actually use

To turn micro‑saving from a nice idea into an automated process, you need a minimal digital stack that removes manual effort. Start with a current account that supports instant notifications and categorisation; this gives you real‑time feedback on what leaves your balance. Layer on one or two of the best budgeting apps rather than ten competing dashboards. In 2021–2023, adoption of envelope‑style and “zero‑based” budgeting apps climbed steadily because they make it obvious where each unit of currency is going. Look for tools that include round‑up savings, goal‑based sub‑accounts and scheduling of recurring micro‑transfers. Many neobanks and brokerage apps now support automatic sweeps into a high‑yield savings or low‑risk investment product whenever your balance exceeds a configurable threshold, which is a direct, passive way to capture surplus cash before you spend it.

Beyond core banking and budgeting, coupon and cash‑back plugins for your browser, as well as loyalty apps for the shops and services you actually use, are essential components of a micro‑saving toolkit. Between 2021 and 2023, large issuers and retailers expanded their cash‑back programs, and aggregate industry reports show billions in unused rewards every year; that is lost free money. Installing one or two reputable extensions that automatically apply discount codes, plus a cash‑back portal that routes your normal online purchases, converts your everyday spending into a stream of small rebates. Combine that with digital bill‑management services that scan for unused subscriptions and tariff optimisers for utilities and mobile plans, and you have an integrated, semi‑automatic infrastructure capturing micro‑savings without manual vigilance.

Offline helpers: physical anchors that make saving visible

Even with strong digital tools, it helps to have physical cues that reinforce the behaviour. A basic example is an old‑fashioned change jar, but you can upgrade the concept: use a transparent container near your front door specifically labelled for a concrete goal, such as “Three‑month buffer” or “Travel fund”. Visibility matters; behavioural experiments have shown repeatedly that physical prompts increase adherence to financial routines. Low‑tech but high‑impact tools include printed habit trackers on the fridge, simple envelopes for recurring cash categories like groceries or fuel, and a one‑page “spend rules” sheet posted near your workspace. These act as persistent reminders to execute micro‑saving rules, like rounding down each cash purchase or parking every unexpected refund into savings instead of general spending.

For people who prefer tactile systems, the classic envelope method remains one of the most underrated frugal living tips to save money. You allocate cash into category envelopes at the start of the period and implement micro‑rules such as skimming a small percentage off the top of each envelope into a dedicated savings envelope. When it is empty, that category is done; you are enforcing a hard budget constraint mechanically, without relying on apps. Over 2021–2023, several studies on cash‑stuffing trends in social media communities documented that even modest income households were able to build meaningful emergency funds using this approach. Physical boundaries and visual feedback make each minor sacrifice feel purposeful instead of like vague deprivation.

Step‑by‑Step Process: Building a Micro‑Saving System

Step 1: Map your cash flow in detail

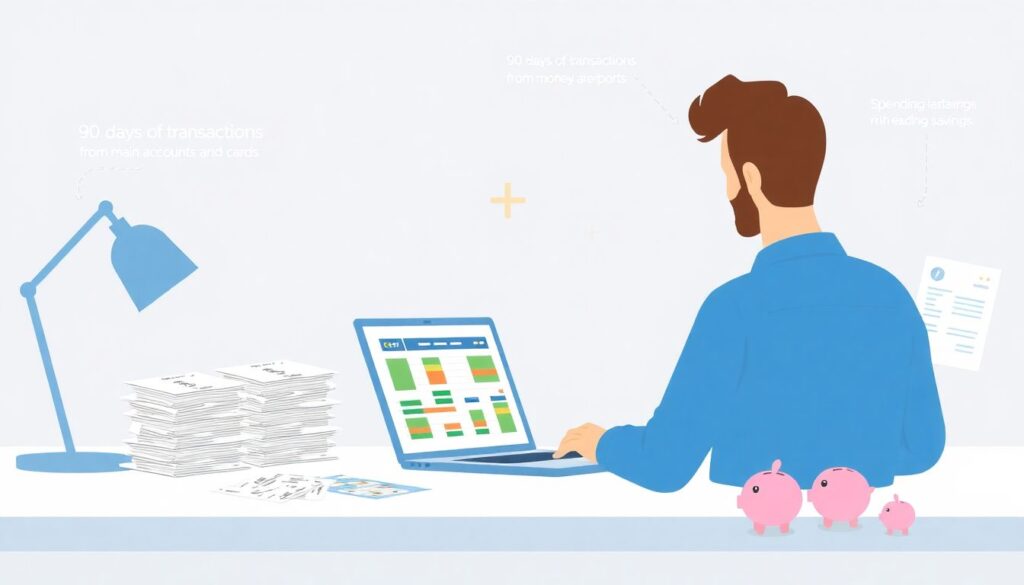

Before you can implement micro‑saving, you need a detailed view of where your money currently leaks away. Export the last 90 days of transactions from your main accounts and cards; most institutions support CSV downloads. Load this into your budgeting app or a spreadsheet, then segment spending into high‑level categories such as housing, food, transport, subscriptions and discretionary. Over 2021–2023, analysis from various personal finance platforms consistently showed that “small, frequent” transactions—coffee, snacks, convenience fees, micro‑subscriptions—made up a surprisingly large share of variable spending, often 15–25% for urban users. These high‑frequency, low‑amount items are precisely where micro‑saving can be most powerful, because these charges are easy to trim or reroute with tiny habit tweaks that do not feel like major sacrifices.

Once you have the baseline, mark three types of entries: fixed obligations you cannot easily change in the short term, flexible necessities where you can probably optimise prices, and pure discretionary outflows. From here, define a few quantitative micro‑saving targets. For example, you might aim to reclaim 5% of food spending through a mix of meal planning and loyalty rewards, 10% of subscription spending by cancelling or downgrading, and a flat amount—say $1–$3—skimmed from each discretionary purchase over a certain threshold. This transforms abstract money saving tips into explicit, testable rules. At this stage, micro‑saving is less about immediate restriction and more about establishing the measurement layer so that upcoming changes can be tracked and iterated like a simple engineering experiment.

Step 2: Automate tiny saves so you can forget about them

With your cash flow mapped, the next phase is to hard‑wire micro‑savings into your system so that they run without constant attention. Activate round‑ups on your main debit card if your bank offers it: every payment gets rounded to the nearest whole unit and the difference is moved to a savings pot. Product analytics published by several neobanks between 2021 and 2023 indicate that active round‑up users quietly accumulate hundreds per year, even at modest transaction volumes, simply because the micro‑amounts are psychologically invisible. Add scheduled micro‑transfers—perhaps a small amount every weekday morning—into your savings account. If you are wondering how to save money fast without feeling a painful cut, stacking several such automated streams is one of the most effective approaches.

For recurring bills and subscriptions, set up a rule that any time an expense is reduced—by switching providers, negotiating a lower rate or cancelling altogether—the difference between the old and new amounts is automatically routed into savings. Many people renegotiate a contract, enjoy the lower bill and then let the freed money dissolve into other spending; a micro‑saving system captures that delta permanently. Some banking and savings apps let you attach “boosts” based on triggers, such as transferring a small amount into savings every time you receive a notification for dining out. Even if it is just a few units, this creates a behavioural link: discretionary spending now has a built‑in savings tax, turning lifestyle choices into funding for your future self.

Step 3: Optimise routines and spending patterns

Once the automated layer is in place, move to behavioural optimisation—tweaking daily routines so they inherently produce small surpluses. Examine recurring micro‑decisions: coffee, transport, lunch, digital rentals, fees for convenience services. Micro‑saving is rarely about cutting these out entirely; it is about designing cheaper defaults. For example, switching two café visits per week to home‑brewed coffee, while immediately transferring the price difference into savings on each occasion, converts a vague intention into a repeatable protocol. Over a year, such pairs of choices can add up to hundreds. This is where classic frugality advice becomes more systematic: you are encoding frugal living tips to save money into a set of if‑then rules attached to specific contexts in your day.

Periodic reviews close the loop. Once a month, perform a short retrospective in your app or spreadsheet: how much did automation capture, and which micro‑behaviours contributed most? Between 2021 and 2023, users of digital savings tools who conducted even brief monthly reviews had significantly higher retention and savings balances, according to industry whitepapers, because feedback reinforces the connection between tiny actions and visible results. If some habit changes feel too painful or unsustainable, redesign them instead of giving up on the whole system. For example, if bringing lunch from home daily fails after two weeks, try a hybrid model of three days packed, two days out, and make sure the savings from those three days are explicitly transferred. Over time, these iterative adjustments turn your ruleset into a personalised engine that consistently generates incremental surpluses.

Troubleshooting: When Micro‑Saving Stops Working

Common failure modes and how to detect them

Any system that runs in the real world is going to drift, and micro‑saving is no exception. One frequent failure mode is “invisible gains”: users do a lot of small saving actions, but the money merges back into the main account, so there is no separate, growing balance to reinforce the habit. The fix is structural: maintain at least one dedicated savings or investment account where all micro‑transfers, round‑ups and rebates are funnelled and never mixed with daily spending. Another common issue, visible in many budgeting datasets from 2021–2023, is subscription creep: people run a “clean‑up sprint”, cancel several services, feel accomplished, and then slowly add new recurring charges until they exceed the original level. Implementing a rule that any new subscription requires a matching cancellation or an automatic increase in savings preserves the surplus instead of allowing gradual inflation.

There is also the psychological backlash problem: if micro‑saving rules feel like constant friction—too many decisions, too many restrictions—people tend to abandon them after a few weeks. Watch for signs such as regularly overriding your own rules, feeling resentful about every transfer, or starting to treat saved money as “found cash” that can be spent impulsively. When this happens, the troubleshooting approach is to simplify. Reduce the number of active rules, keep only the highest‑yield, lowest‑pain ones and increase automation so that fewer choices rely on willpower. This is where using one or two carefully chosen money saving tips is better than juggling dozens. You can also introduce positive reinforcement, like allowing a small, guilt‑free treat when you hit a micro‑milestone, to keep motivation aligned with long‑term goals.

Adjusting, scaling up and dealing with setbacks

A robust micro‑saving system is not static; it should adapt as your income, expenses and priorities change. After three to six months, examine your data and consider incrementally increasing the size of automatic transfers or the intensity of certain rules. For example, you might raise round‑up levels, or add a percentage‑based skim on income inflows, so that when your earnings grow, your savings rate scales automatically instead of allowing lifestyle creep to absorb the difference. Over 2021–2023, financial planners increasingly recommended such mechanisms because clients who tied their savings rate to income changes were more likely to maintain progress through economic volatility. In effect, you are building dynamic ways to save money each month that evolve with your real‑world context, instead of freezing your system at a single configuration.

Setbacks are inevitable: surprise expenses, job changes, periods of higher bills. When an emergency forces you to pause or reverse some savings, treat it as a planned use of your financial buffer, not as a failure. The key troubleshooting move is a structured reboot. Once the shock passes, explicitly restart your micro‑saving rules, even at a lower level if needed, rather than waiting for a vague “better time”. If you need to accelerate recovery, consider short, time‑boxed pushes: temporarily increase micro‑transfers or add a couple of extra constraints for 30–60 days. This is a controlled version of how to save money fast without flipping your lifestyle upside down indefinitely. Over the long term, the compounding of these tiny, mostly automated behaviours matters far more than any single intense month or setback, and that is precisely why micro‑saving is such a resilient, realistic strategy in the economic conditions of the last few years.