Why your utilization rate moves the needle

Credit utilization is the share of revolving limits you’re actually using, and bureaus treat it as a core risk signal. In most scoring models, amounts owed account for roughly 30% of your FICO score; utilization is the biggest slice there. Keep it below 30% for stability and under 10% for elite scores. Lenders read high ratios as stress, even if you never miss payments. The best credit utilization ratio is the one you can sustain month to month without cash‑flow gymnastics, because consistency matters as much as the absolute number.

Quick wins that work in the real world

Start with balances you can shrink today. Make an extra mid‑cycle payment so the statement reports lower debt; many issuers snapshot 3–5 days before your close date. Shift small recurring charges to a debit card for a month to let accounts cool down. If you have multiple cards, spread spending to avoid any one line exceeding 30%. These tactics are how to lower credit utilization without changing your lifestyle, and they often move scores within one or two reporting cycles.

Technical details: how utilization is computed

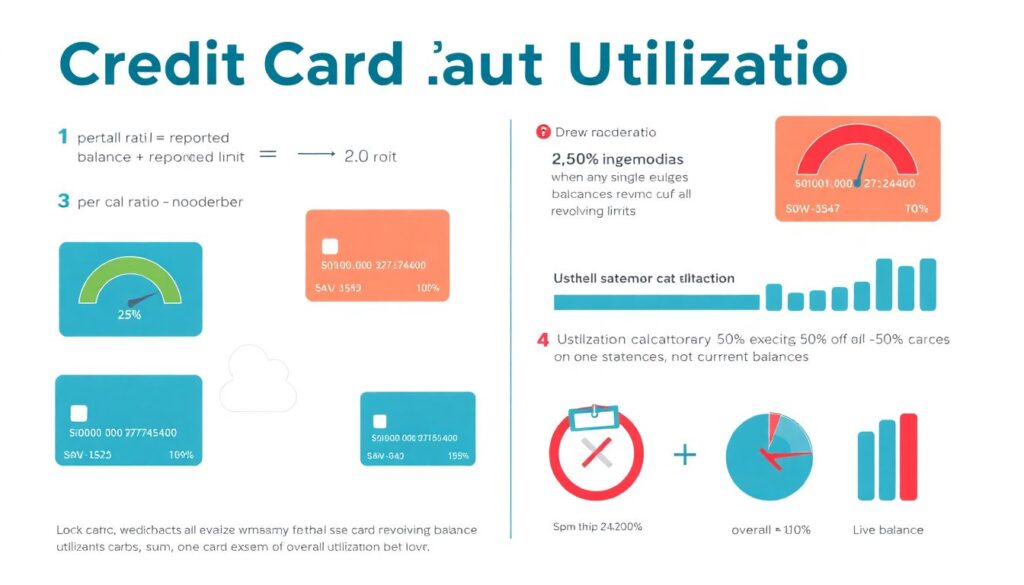

– Per‑card ratio = reported balance / reported limit; overall ratio = sum of all revolving balances / sum of all revolving limits.

– Scoring models can penalize when any single card tops ~50%, even if overall stays low.

– A credit utilization calculator uses statement balances, not current balances, unless the issuer reports daily (rare).

– Closed cards with a balance have no limit, often counted as 100% on that line until paid.

– Authorized user lines typically count, but some models de‑weight thin AU histories.

Timing beats effort: pay before the snapshot

Your payment date and your reporting date are not the same. If your card closes on the 20th, a payment on the 19th lowers the number bureaus see; a payment on the 22nd helps cash flow but not this cycle’s metrics. Set calendar reminders one week before each statement close, then push enough to drop below the target threshold. Many clients see a 20–40 point swing in 30 days simply by changing the cadence, no extra dollars required.

Expand limits, don’t expand spending

Requesting a higher limit lowers the ratio’s denominator instantly. Ask issuers for a soft‑pull increase every six months, especially after income changes. Phrase the request as “account review” to avoid an unnecessary hard inquiry. If granted, keep usage steady; the goal is to increase credit limit to lower utilization, not to fund new expenses. For thin files, adding a second no‑fee card can reduce volatility and smooth month‑to‑month reporting.

Technical details: underwriting realities

– Soft‑pull CLI: common with Amex, Capital One; hard‑pull more likely with Chase, Citi. Always confirm before proceeding.

– Typical successful CLI asks range 10–30% of current limit; larger jumps need documented income.

– A single hard inquiry usually costs 3–8 points and fades in ~6 months; limits, however, persist in your profile.

– New cards shorten average age; offset by keeping old lines open and fee‑free.

– Don’t lower limits or close cards right before a mortgage pre‑approval window.

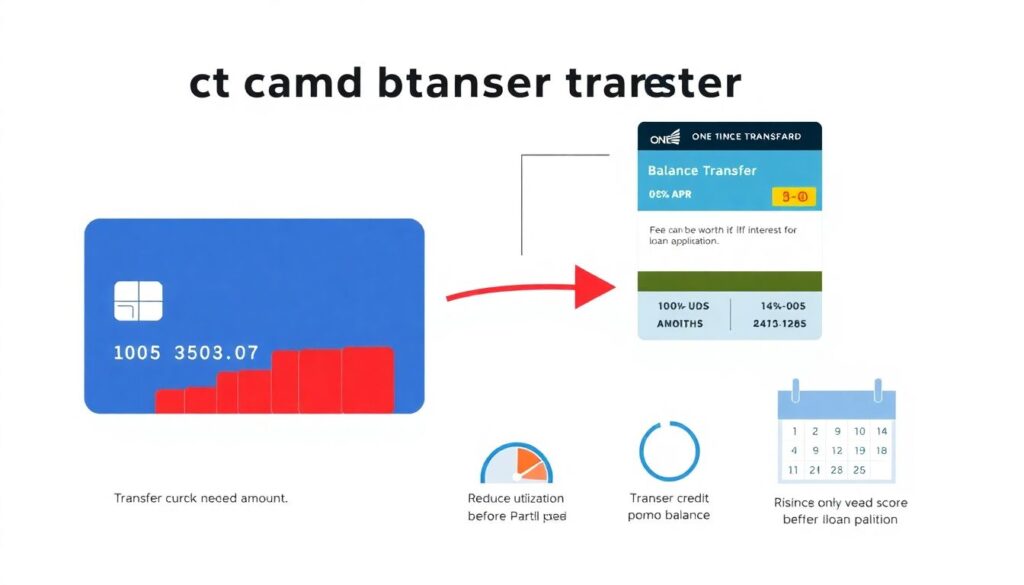

Move balances the smart way

If one card is maxed but others sit idle, a one‑time reallocation helps. Consider balance transfer credit cards with 0% APR for 12–21 months and a 3–5% fee; the fee can be worth it if interest is higher or if utilization is choking your score before a loan application. Transfer only what’s needed to push each card under 30%, then automate payoff during the promo. Avoid purchases on the promo card; mixed balances can forfeit grace periods.

Field notes: two quick case studies

A freelancer carried $2,400 on a $3,000 limit (80%). By splitting spend across two new no‑fee cards and paying $600 mid‑cycle, her per‑card ratios fell under 30%, and her score rose 32 points in five weeks. A teacher with three cards timed payments to two days before statement close and used a small CLI on the oldest account; overall utilization dropped from 42% to 18% without extra cash outlay, cutting his auto loan APR quote by 1.1 percentage points.

Technical details: measurement and tools

– Use a credit utilization calculator with statement close dates to project next month’s ratios.

– Track “all‑zero except one” (AZEO) when prepping for underwriting: keep one card reporting 1–9%, others zero.

– Revolving limits include bankcards and most retail cards; charge cards often report “no preset limit” and are model‑dependent.

– Experian, Equifax, TransUnion may update on different days; expect staggered changes.

– Beware installment loans: they don’t affect utilization, but new debt can sway underwriting.

Pitfalls to avoid while optimizing

– Don’t pay to zero then immediately reload the same card before the statement closes; you’ll look maxed again.

– Avoid consolidating all spend on a single rich‑rewards card during a mortgage window; per‑card spikes hurt.

– Skip limit decreases or product closures until you’ve secured any upcoming financing.

– Don’t ignore small store cards; a $200 balance on a $500 limit is a problematic 40% even if overall is low.

– Keep utilization low for at least 90 days before major applications to stabilize your range.