Why a truly global lens matters in 2025

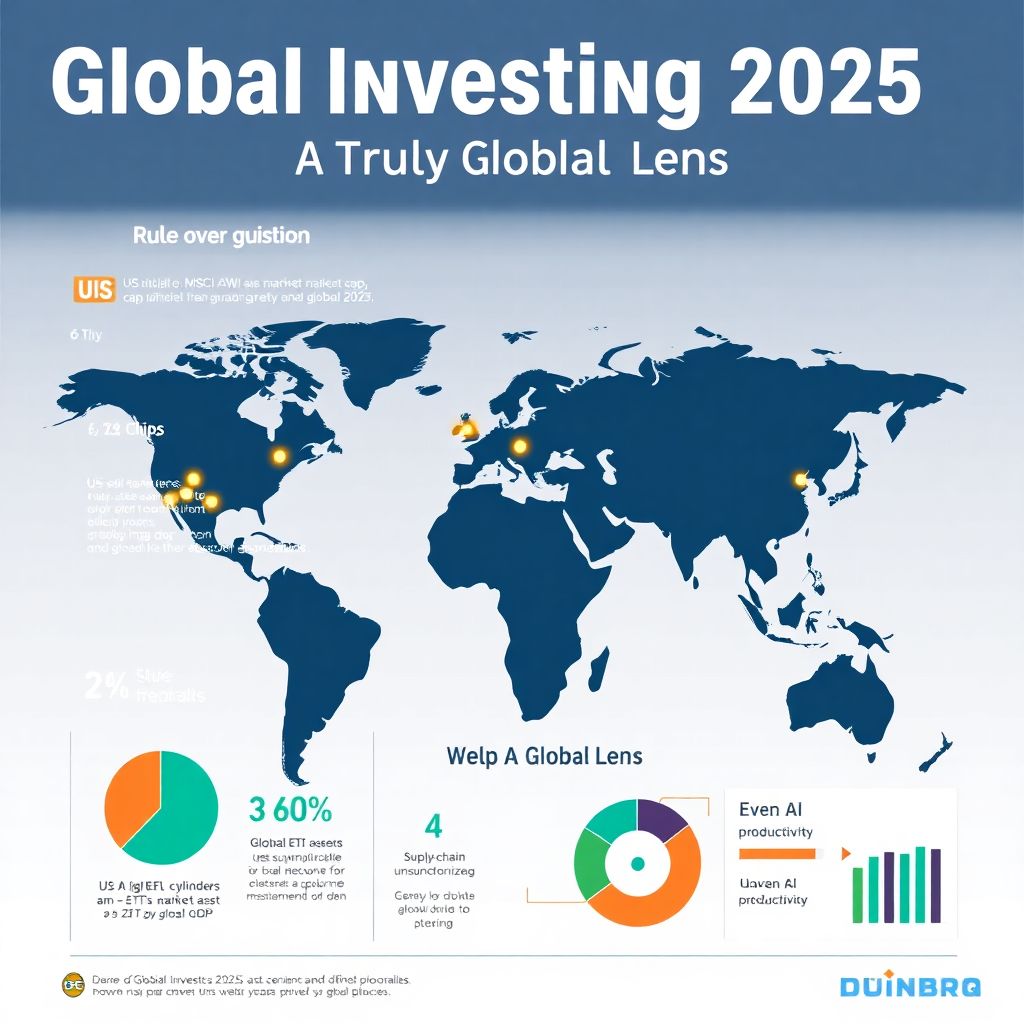

A decade ago, staying mostly in domestic assets could be excused by home‑bias comfort and plentiful tech-led returns in the U.S. Today, concentration risk is palpable: by late 2024, the U.S. represented roughly 60% of MSCI ACWI by market cap, yet only about a quarter of global GDP. Meanwhile, global ETF assets surpassed $12 trillion in 2023 and kept expanding in 2024, signaling a durable shift toward low‑cost diversification. If you’re shaping a global investment strategy in 2025, you’re balancing three realities—rate cycles that are no longer synchronized, supply‑chain rewiring, and uneven productivity gains from AI.

Put simply, the world’s return engine has multiple cylinders again.

Data snapshot: where the risk and return have been

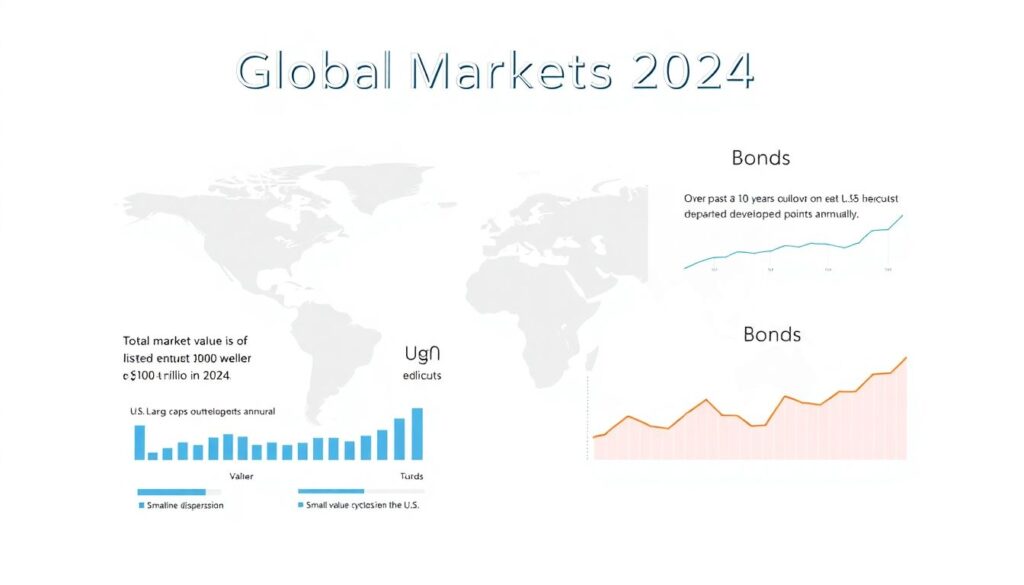

– Global equities: The total market value of listed equities hovered well above $100 trillion by 2024. Over the past 10 years, U.S. large caps outperformed developed ex‑U.S. by 3–5 percentage points annually, but factor dispersion widened, and small-value cycles resurfaced outside the U.S.

– Bonds: After the 2022–2023 reset, starting yields turned positive again as predictors of medium‑term returns. Global aggregate bond yields in many developed markets normalized to the 3–4% range by 2024, improving forward return math relative to the post‑GFC era.

– Emerging markets: EM share in MSCI ACWI sits around the low teens; however, EM accounts for the majority of global GDP growth in purchasing‑power terms. Volatility remains higher, but currency-adjusted earnings growth has been competitive in Asia.

That’s the backdrop for building, not guessing.

Core principles for a durable plan

When people ask how to invest internationally, I start with three evidence‑based ideas: diversify by risk drivers (not flags on a map), tie risk to your spending horizon, and pay for what you can’t easily replicate. Costs, taxes, and behavior will matter more than headline narratives over a 10‑year window.

And yes, simplicity scales better than complexity.

From principle to practice: a global asset allocation strategy

A global asset allocation strategy should map growth, income, and inflation protection to instruments you can hold through full cycles. That means leaning on broad indexes for core exposure and using active or factor tilts where markets are less efficient or where strategic themes (like onshoring or energy transition) create pricing gaps.

If your allocation can’t survive a normal recession, it isn’t strategic—it’s a hunch.

The building blocks

Equities: the growth sleeve

For most long-term investors, global market-cap exposure is the anchor. The best global index funds and total-market ETFs provide instant breadth at sub‑0.10% expense ratios. ACWI‑like cores can be complemented with targeted sleeves: developed ex‑U.S. for valuation diversification, and emerging markets ETFs for demographic and productivity beta. Consider factor overlays (quality for balance‑sheet strength; value for mean reversion) outside the U.S., where dispersion is larger.

Remember, concentration risk is a risk factor. Don’t let a single country or sector write your entire equity story.

Fixed income: the ballast

Global core bonds hedge equity drawdowns and finance future rebalancing. With higher starting yields, hedged developed‑market bonds make more sense for USD or EUR investors who want rate diversification without the full brunt of currency swings. Unhedged exposure can diversify over the long run, but currency can account for over half of short‑term volatility in global bond sleeves.

Think of bonds as your dry powder, not your performance trophy.

Real assets and alternatives: inflation and correlation puzzles

Listed infrastructure, global REITs, and commodities futures can help when supply shocks or policy shifts reprice inflation risk. Allocations of 5–15% combined are typical for diversified portfolios. Liquidity matters: if you can’t rebalance during stress, the hedge may not hedge when needed.

Small doses, clear roles.

A step-by-step playbook you can actually follow

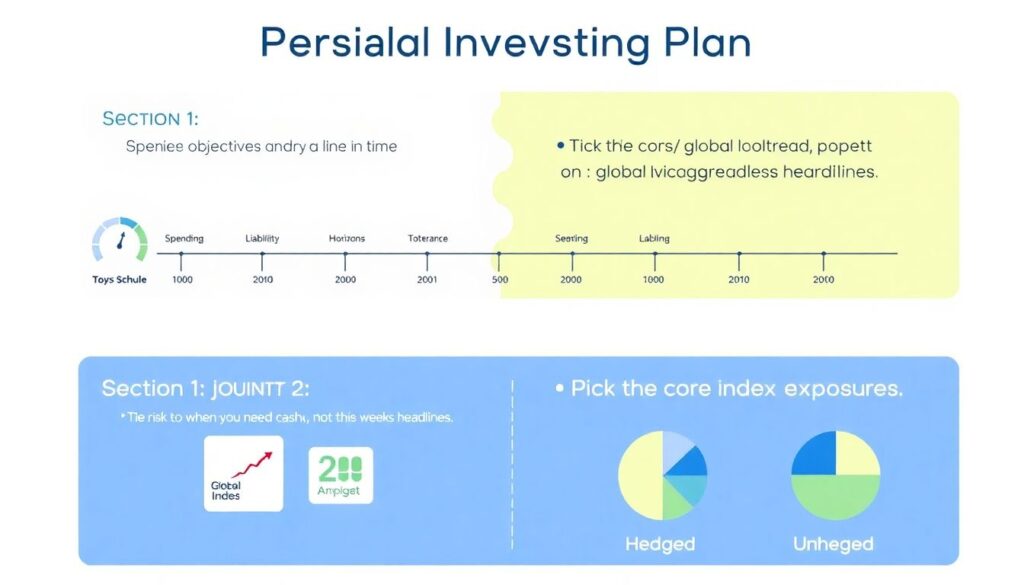

1) Define objectives and draw a line in time

– Spending schedule, liability horizons, and drawdown tolerance. Tie risk to when you need cash, not to this week’s headlines.

2) Pick the core index exposures

– Use a low-cost global equity fund plus a global aggregate bond fund (hedged or unhedged by design). This anchors the global investment strategy to broad market betas.

3) Add deliberate tilts

– Developed ex‑U.S. value or quality, small caps, and selective emerging markets ETFs where governance and earnings quality score well. Keep each tilt sized (e.g., 5–15%) and review annually.

4) Set rebalancing and cash rules

– Calendar or bands (say, 20% of target weight). Automate contributions and withdrawals to enforce discipline.

5) Control what you can: fees, taxes, and slippage

– Prefer vehicles with tight spreads and deep liquidity. Use limit orders for thin markets and avoid trading at local market opens.

6) Stress test and scenario‑plan

– Model a 20–30% equity drawdown, a 200 bps rate shock, and a 10% currency move. If you won’t hold through these, resize.

7) Document policy and review annually

– A one‑page IPS beats a shelf of “hot takes.” Update only when goals or constraints change.

Costs, taxes, and operational realities

Fees compound in reverse. A 50 bps drag over 10 years can erase a year of contributions for many savers. In taxable accounts, favor ETFs for in‑kind redemption mechanics where available, harvest losses opportunistically, and place income‑heavy assets in tax‑advantaged wrappers when possible.

Your edge might just be frugality plus patience.

Currency and domicile choices

Hedging decisions should be intentional. Equity currency exposure often diversifies shocks to domestic income; bond currency exposure often adds avoidable volatility. Fund domicile influences withholding taxes on dividends; check treaty rates and whether your broker provides relief at source.

Small legal details, big cash-flow consequences.

Forecasts for 2025–2030: base case and alternatives

The base case going into 2025 assumes gradual disinflation with uneven pacing across regions, enabling cautious policy easing by major central banks. Under that path, expected nominal returns cluster around: global equities 6–8% annualized (range-wide by valuation starting points), developed core bonds 3–5% with positive term premia, and real assets offering episodic protection against supply‑side shocks.

Two alternative scenarios deserve airtime. First, a productivity upswing from AI diffusion that lifts developed‑market trend growth by 0.3–0.6 percentage points, especially in tradable services. That would favor quality and cash‑flow compounders globally and could extend multiples in markets with strong IP protections. Second, a stickier‑inflation regime from deglobalization and industrial policy overlaps, keeping policy rates higher for longer; under that path, short‑duration credit, value cyclicals tied to capex, and inflation‑sensitive assets would lead.

Forecasts are ranges with error bars—positioning should be resilient, not clairvoyant.

Regional notes you can use

– U.S.: Earnings breadth remains narrow but is slowly widening beyond mega‑caps; margins depend on wage moderation and cloud capex cycles.

– Europe: Valuations discount low growth; higher buyback activity and energy transition capex could surprise on the upside.

– Asia ex‑Japan: Structural growth anchored by supply‑chain relocation and domestic consumption in India and Southeast Asia; governance selection remains key.

– Japan: Corporate reforms and improving return-on-equity trends justify sustained foreign inflows, with currency a major swing factor for returns.

None of these are guarantees, but each shapes position sizing.

Industry impact: what shifts as investors go global

As global allocations normalize, fee pressure intensifies. Scale will keep pushing the best global index funds toward razor‑thin pricing, while active managers migrate to capacity‑constrained niches (small caps, frontier markets, event‑driven credit) where skill can surface. Expect more cross‑border portfolio solutions embedded in retirement plans and model portfolios, blurring the line between “domestic first” and “global default.”

Distribution is changing too: digital platforms increasingly pre‑package a global asset allocation strategy for retail investors, with automated rebalancing and tax‑loss harvesting. The operational moat is data and execution, not glossy brochures.

Technology, data, and regulation

Better tick‑level data and AI‑assisted analytics widen the gap between disciplined process and gut feel. On the regulatory side, sustainability disclosure regimes are converging, but taxonomy fragmentation persists; it will shape how global mandates report exposures, especially in emerging markets. Liquidity rules and swing pricing in funds should dampen run risk during stress, but investors still need their own liquidity buckets.

Plumbing matters when the music stops.

Putting it all together

A well-built global portfolio in 2025 is boring by design: broad cores, intentional tilts, explicit rules. It answers how to invest internationally without turning you into a full‑time trader. It also acknowledges that risk is a budget, not a wish list, and that rebalancing is your quiet superpower.

Stay diversified, keep fees microscopic, and let time—not headlines—compound your edge.