You don’t get paid what your contract says—you get paid what lands in your account after taxes and deductions. That gap is where most beginners stumble. They confuse gross with net, forget pre-tax benefits, and misread pay periods. One week they celebrate a raise; the next, their take-home shrinks because withholding changed. Before you negotiate anything, map your cash flow with a paycheck calculator so you don’t anchor on a fantasy number. Common rookie mistake: assuming tax brackets apply to your whole salary. They’re marginal. Another: ignoring city or local taxes that quietly trim your check. If your budget fails, it’s usually because you planned for gross, not reality.

Real cases: where the money actually goes

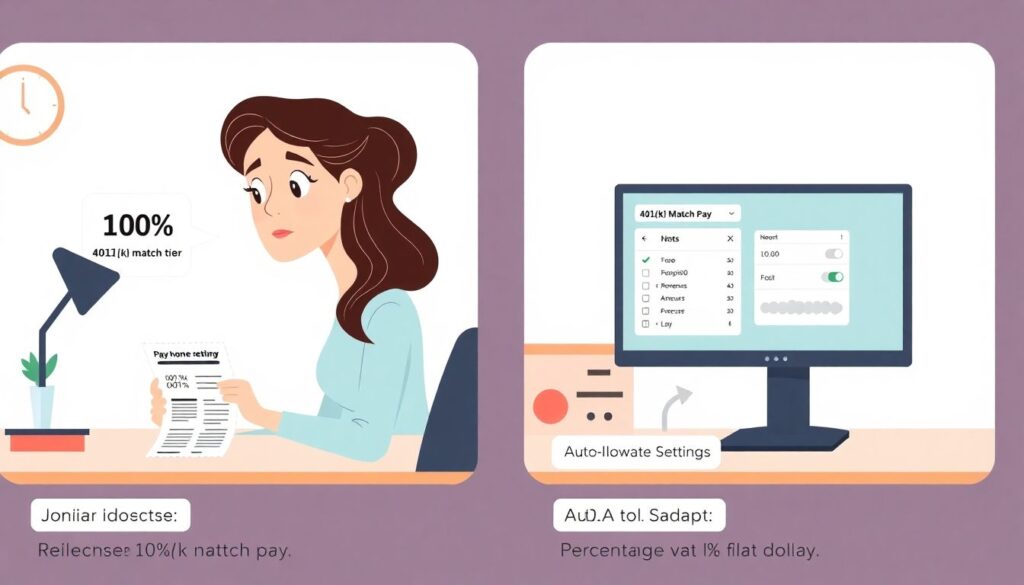

I worked with a junior designer who thought a 10% raise would fix her budget. It didn’t. Her employer bumped her into a higher 401(k) match tier, and she auto-escalated contributions without noticing. Her take-home fell despite the raise. Once we tuned her deferral to a flat dollar amount, not a percentage, her net stabilized. Another case: a contractor got “paid more” but brought home less after switching to biweekly billing with higher self-employment tax. He used a take-home pay calculator and realized quarterly estimated taxes were starving his cash flow; shifting to monthly estimates plus a separate tax savings account restored predictability.

Non-obvious solutions to boost net pay

Most people hunt for a bigger salary, but hidden levers sit in your deductions. Move what you can into pre-tax buckets: transportation benefits, HSA for high-deductible plans, and FSA for dependent care—each lowers taxable income without a lifestyle hit. Fine-tune your W-4 with a tax withholding calculator instead of guessing allowances; small changes can stop over-withholding that locks up cash until refund season. If your employer offers supplemental pay (bonuses, commissions), ask payroll to use aggregate withholding rather than flat methods when permissible; the method can materially change your net in the bonus month.

Alternative methods: planning beyond payroll

If your income is lumpy, a salary after tax calculator won’t capture timing risk. Build a “pay yourself” system: route all income into a holding account, then auto-transfer a fixed “salary” twice a month. That artificial paycheck smooths volatility and enforces discipline. Freelancers should treat taxes as a cost of goods sold—skim a set percentage of every invoice into a tax-only account the moment it clears. When benefits are thin, replicate them: open an HSA if eligible, set up a solo 401(k), and compare IRAs. Use a net pay calculator to model how each contribution shifts today’s cash versus future tax savings.

Pro tips that separate pros from beginners

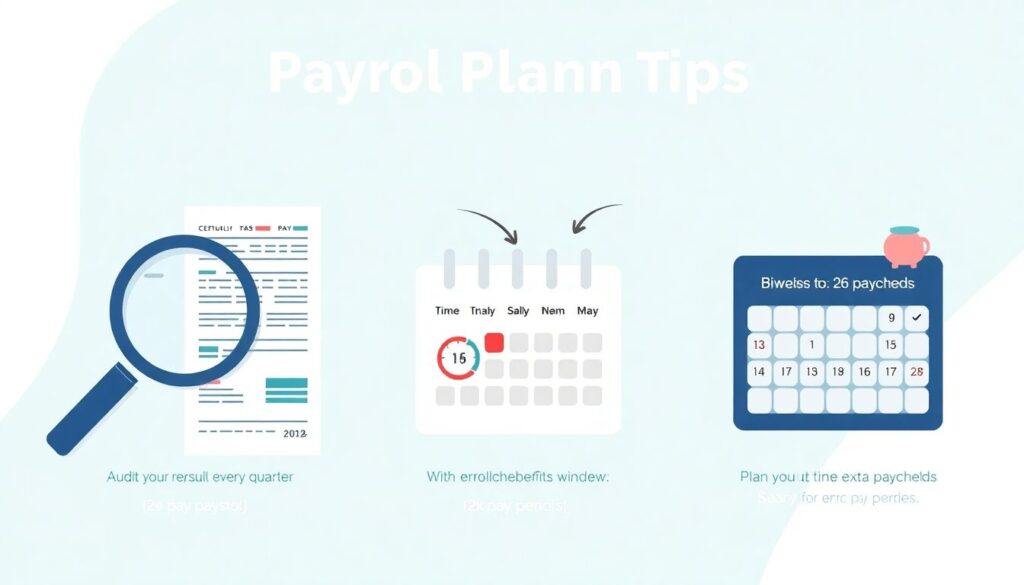

– Audit your paystub line by line every quarter; errors happen, especially after open enrollment or promotions.

– Time raises to benefits windows; increasing pay before adjusting withholdings can trigger unpleasant surprises.

– If you’re paid biweekly, plan for the two “extra” paychecks a year; assign them to debt or savings in advance.

– Test drive changes with a take-home pay calculator before filing new forms.

– When moving cities, rerun your numbers with local taxes and mandatory benefits.

– Keep a one-page playbook: deductions, elections, and contacts in payroll—so fixes take minutes, not weeks.

Common beginner mistakes you can avoid

Newcomers chase the headline number and skip scenario analysis. They misclassify filing status, leading to the wrong withholding. They rely on refunds as forced savings and ignore cash drag all year. They forget that pre-tax contributions can reduce FICA exposure only in limited cases, confusing 401(k) with cafeteria plans. They mix up pay frequency with a pay raise and blow the third check months. They never reconcile PTO payouts, overtime rules, or benefit premiums midyear. All of this is fixable if you run your numbers with a net pay calculator and keep your W-4 aligned with life changes.

Tools that actually help, not just impress

Use a take-home pay calculator to test “what if” scenarios before you commit: new city, different deductible, adding a dependent, or shifting a bonus month. Pair it with a salary after tax calculator to compare offers across states without spreadsheet acrobatics. For precision, a tax withholding calculator lets you model W-4 adjustments so your check matches your plan. When you need a quick gut check, a stripped-down paycheck calculator is faster than your HR portal and great for sanity checks after promotions or benefit changes.

When to talk to payroll and when to call a pro

Ping payroll if your deductions don’t match elections, if a bonus was taxed unexpectedly, or if a new locality tax appears after a move. Ask how they handle supplemental wage withholding and whether they can run a test payroll. Call a tax pro when you have multiple states, equity comp, or self-employment layered onto W-2 income. A short consult can prevent a big April bill and keep your take-home predictable throughout the year.

The bottom line

Your take-home is a system outcome, not a mystery. Treat it like a product: instrument it, iterate, and ship improvements every quarter. Model first, file second, confirm with your paystub, and capture the gains in your budget immediately.