Why Parents Feel Crushed by Debt (And Why This Guide Is Different)

Parenthood changes how you think about debt.

It’s no longer just about numbers. It’s about rent or mortgage, daycare, groceries, school trips, medical bills, and the low‑grade anxiety of “what if something happens to my job?”

This guide walks through the debt snowball vs. avalanche methods step by step, but with a twist: we’ll plug them into a real family context, add risk management, and mix in a few non‑obvious strategies most basic “budget blogs” never mention.

You’ll see practical steps, warnings about common traps, and specific tips for beginners who are juggling kids, time, and energy—not spreadsheets for fun.

—

Step 1: Map Your Debt Like an Engineer, Not Like a Panicked Parent

List Every Debt with Technical Precision

Start with a complete “debt inventory.” Treat this as an engineering spec, not a vague list.

For each debt, write down:

1. Creditor name (e.g., Visa, auto loan, student loan)

2. Balance

3. Interest rate (APR)

4. Minimum monthly payment

5. Due date

6. Whether it’s secured (backed by collateral like a car or house) or unsecured

Use a simple spreadsheet or notes app. It doesn’t have to look pretty; it has to be accurate.

Short on time? Break it into two evenings:

– Night 1: Credit cards and personal loans

– Night 2: Student loans, car, medical, buy-now-pay-later, and any “forgotten” store cards

Beginner Warning: Don’t Rely on Memory

A common beginner mistake is estimating balances and interest rates “from memory.” That leads to bad math and false optimism.

Log into each account or open the latest statement. If you’re too tired to finish, stop—but don’t guess. Incomplete data is worse than no data.

—

Step 2: Set a Realistic “Cash Flow Fence” Around Your Family

Stabilize Before You Attack

Before deciding the best method to pay off credit card debt fast, you need a stable monthly surplus—money that can be aimed at debt without risking food, rent, or essential childcare.

Do this:

1. Calculate your average monthly take‑home pay (last 3 months).

2. List fixed “survival” expenses: housing, utilities, basic groceries, transportation, essential childcare, minimum debt payments.

3. Add a small line item for kid‑related “surprise but not really” costs (birthday gifts, field trips, school supplies).

Your goal:

Income – Survival Expenses = Consistent Surplus

If your surplus is less than $150 a month, pause here and consider adjustments:

– Negotiate bills (phone, internet, insurance).

– Remove or downgrade subscriptions.

– Temporarily cap kid activities (e.g., limit to one paid activity per child).

This is the cash flow fence: you’ll attack debt aggressively, but never by robbing the “family essentials” side of the fence.

Unconventional Angle: Protect a Tiny “Sanity Budget”

Total deprivation backfires for parents. Kids feel the stress, and adults compensate with impulse spending.

Keep a small sanity budget (even $20–$40/month) for low-cost treats or family fun. It slows payoff slightly but dramatically improves the odds you’ll stick with the plan.

—

Step 3: Debt Snowball vs. Avalanche – Understand the Mechanics

Debt Snowball: Emotional Momentum Engine

Definition:

You pay minimums on all debts, then put every extra dollar toward the smallest balance first, regardless of interest rate. Once that’s gone, you roll its old payment into the next smallest balance. The payment grows like a snowball.

Pros (especially for parents):

– Quick psychological wins when a debt disappears

– Fewer accounts to track over time

– Great if both partners struggle with consistency or ADHD

Cons:

– You may pay more total interest than with avalanche

– Mathematically sub‑optimal in pure financial terms

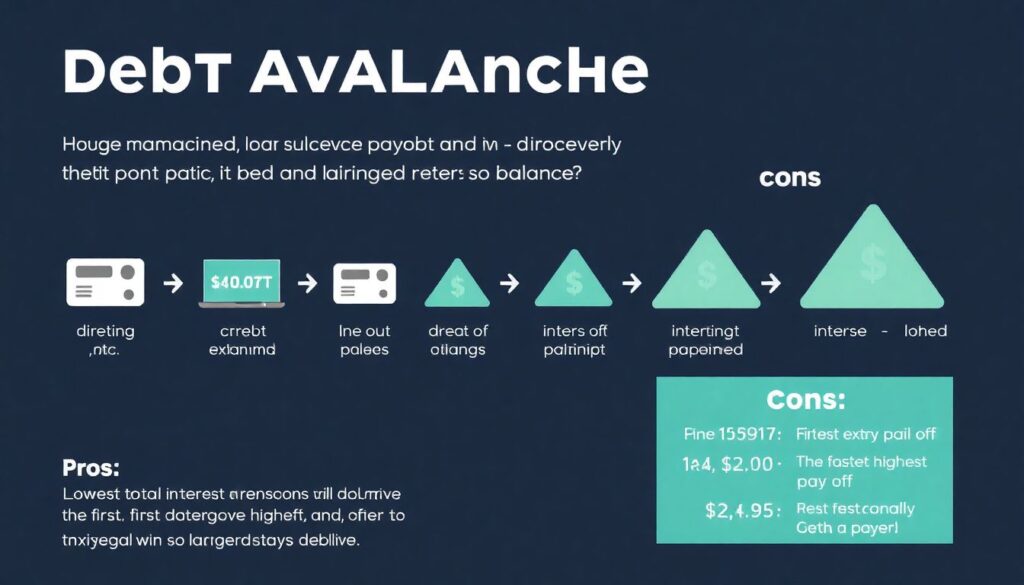

Debt Avalanche: Interest Rate Optimization

Definition:

You pay minimums on all debts, then direct every extra dollar to the highest interest rate first, regardless of balance. When that’s killed, move down to the next highest APR.

Pros:

– Lowest total interest paid

– Often the fastest overall payoff if you stick to it

Cons:

– The first “win” might take months or more

– Emotionally harder when the highest interest debt is also the biggest balance

If you want to experiment without complex math, try a free debt snowball vs avalanche calculator online. Plug in your debts and compare payoff times and interest paid. This gives a concrete sense of the trade‑offs instead of guessing.

—

Step 4: Choose Your Strategy Like a Project Manager, Not a Fan

Decision Framework: Head vs. Heart vs. Household

Use this practical decision rule:

1. If you and your partner are very numbers‑driven and used to sticking to plans, choose avalanche.

2. If you’ve tried to get out of debt before and lost steam, or one partner is skeptical, choose snowball.

3. If you’re unsure, use a hybrid.

Hybrid Strategy for Parents

A useful hybrid:

1. List debts by interest rate (highest to lowest).

2. But if two debts have similar interest rates (difference less than 2%), pay the smaller balance first among those.

You get near‑optimal math while still enjoying faster emotional wins.

—

Step 5: Implement the Plan Step by Step

Practical Execution in 7 Moves

1. Pick the primary method

Decide: snowball, avalanche, or hybrid. Write it down. This is now your “house policy” for debt payoff.

2. Automate minimum payments

Set up automatic payments for at least the minimum on every debt to avoid late fees and credit score damage.

3. Assign a Target Debt

Based on your chosen method, mark one account as the current Target Debt. Highlight it in your notes or rename it “Target – Payoff First” in your banking app notes.

4. Schedule one “big payment” date

Once per month (ideally right after payday), send all your extra surplus to the Target Debt in one shot. One big intentional move beats constant small guesses.

5. Use micro‑payments as “pressure release”

If you get extra money (side gig, tax refund, selling old baby gear), send it immediately to the Target Debt. Don’t let it rest in checking where it can be “accidentally” spent.

6. When one debt dies, simulate its old payment

The moment a debt is fully paid, redirect its old monthly payment to the next Target Debt. Never let that freed‑up cash “rejoin” your lifestyle.

7. Review monthly for 10 minutes

Once a month, verify balances, interest rates, and progress. Keep this short and structured so it doesn’t become a 2‑hour budget argument.

—

Step 6: Avoid the Classic Parent Debt Traps

Trap 1: Treating Kids as a Reason to Stay in Debt

“Travel is important…,” “They deserve a big birthday…,” “Everyone else has…”

You’re not depriving your kids by fixing your finances; you’re removing future instability. Instead of expensive trips now, think in terms of financial runway and options when they’re teenagers.

Unconventional alternative:

Swap expensive experiences for time‑rich, low‑cash rituals: weekly library visits, park “adventure days,” cooking together. These preserve memories without sabotaging your payoff plan.

Trap 2: Ignoring Risk Exposure (Especially Medical and Job Loss)

Parents face a higher probability of sudden expenses—sickness, broken glasses, dental work, car trouble.

Beginner tip:

Before going all‑in on extra debt payments, accumulate a micro‑emergency fund (e.g., $500–$1,500 depending on household size). Yes, this delays payoff slightly. But without a buffer, a single emergency can push you back to credit cards and break your momentum.

Trap 3: New Debt While Paying Off Old

Snowball and avalanche both assume a mostly stable debt balance. New borrowing—even store financing on a “great deal” stroller—resets your progress.

Rule of thumb:

No new consumer debt during payoff, except true emergencies—defined in advance (medical, housing, essential car repair). “Sales,” holidays, and upgrades don’t qualify.

—

Step 7: Smart Use of Tools – Tech and Professionals

Using Calculators and Apps Without Getting Lost

Debt payoff apps and spreadsheets can be useful, but they can also become a form of procrastination.

Use them narrowly:

– Run your numbers once in a debt snowball vs avalanche calculator to choose a strategy.

– Set up one tracking sheet or app dashboard.

– Then spend more energy executing and earning than endlessly re‑modeling scenarios.

When to Bring in Outside Help

If your debt feels unmanageable or negotiations scare you, external support is completely rational.

– Credit counseling services for parents in debt can help you negotiate lower interest, consolidate payments, and build a realistic budget. Look for non‑profit agencies and check reviews and accreditation.

– You can also hire financial coach for debt payoff plan design if you need behavioral support, accountability, and customized tactics. Unlike investment advisors, some coaches specialize in habits and step‑by‑step systems rather than selling products.

If you’re overwhelmed, one session with a competent professional can save months of confusion.

—

Step 8: Consider Strategic Consolidation (Not Just “One Big Loan”)

When Debt Consolidation Makes Sense for Families

For some, debt consolidation for families with kids is a smart intermediate move, but it’s not a magic eraser.

Consolidation can help if:

– Your new interest rate is clearly lower than your current average

– The term is not so long that you pay more total interest

– You commit to not running balances back up on old cards

Examples:

– A personal loan to combine three high‑interest cards

– A 0% balance transfer card (if you can pay it off within the promo window and avoid transfer fees that erase the benefit)

Unconventional twist:

Think of consolidation as creating a “boss battle” debt—one big, clearly defined target—then attack it using avalanche or snowball. But you only win if you permanently close or drastically limit the old credit lines that got you into trouble.

Red Flags with Consolidation

Avoid:

– “No credit check” loans with vague terms

– Home equity loans used to pay off credit cards if there’s a real chance your income is unstable—don’t risk your home to fix shopping habits

– Long payoff timelines (7–10 years) that feel comfortable but keep you in chains

—

Step 9: Non‑Obvious Levers Parents Can Pull

1. Temporary Lifestyle “Sprints,” Not Permanent Austerity

Instead of promising to be frugal for 5 years (which almost never works), use 90‑day sprints:

– For 90 days, reduce or pause non‑essential expenses (eating out, subscriptions, kid extras) and focus that savings on debt.

– After 90 days, restore a limited version of some items, evaluate progress, and decide on another sprint.

Short, intense sprints are more realistic for parents who get burned out easily.

2. Monetize Parenting Assets

Look for ways your existing family setup can create income:

– If you’re already home with your own kids, offer after‑school care for one extra child a few days a week.

– Teach weekend classes based on your skills (music, language, coding) from your living room or online while kids are around.

– Rent out unused baby gear or tools in local parent groups.

This isn’t side‑hustle hype; it’s targeted, realistic use of what you already have.

3. Family‑Level Negotiations Instead of Solo Sacrifice

Don’t silently carry the burden alone. Age‑appropriate transparency with kids can help:

– Simple version: “We’re working hard to pay off some old bills so we can do more cool things later. That means fewer treats for a while.”

– Teen version: Share a simplified version of the plan and goals; ask for their ideas to save or earn.

This turns the process into a team project instead of a secret struggle.

—

Step 10: How to Know It’s Working (Beyond the Balance Numbers)

Track 3 Types of Progress

1. Quantitative

– Total debt balance trending down every month

– Fewer open accounts

– Interest paid month‑to‑month decreasing

2. Behavioral

– You check accounts regularly without dread

– Fewer impulse purchases

– Fewer money arguments with your partner

3. Risk Reduction

– You have at least a small emergency fund

– Bills are on autopay, late fees disappear

– Credit utilization gradually improves, boosting your credit profile

These markers prove that the system is working even when that big credit card balance still looks intimidating.

—

Putting It All Together

You don’t need the “perfect” method. You need a workable method that survives real life with kids, fatigue, surprise expenses, and limited time.

In condensed form, your path looks like this:

1. Map every debt with precision.

2. Build a basic cash flow fence and micro‑emergency fund.

3. Choose snowball, avalanche, or a hybrid based on your psychology, not internet arguments.

4. Execute with automation, one Target Debt at a time.

5. Avoid new consumer debt and common parent traps.

6. Use tools—calculators, apps, consolidation—strategically, not emotionally.

7. Pull non‑obvious levers: sprints, monetizing your reality, family buy‑in.

Over time, the chaos of multiple debts converts into a single, clear process. And that clarity, more than any specific tactic, is what gives your family back its financial breathing room.