Why Budgeting Matters More Than the Deal Itself

Most new investors obsess over “the deal” and forget the boring part: the budget. But every seasoned landlord will tell you the same thing: your numbers make or break your rental property investment strategy, not the granite countertops.

If you know exactly how to budget for rental property before you buy, you can:

– Avoid negative cash flow surprises

– Survive vacancies and repairs without panic

– Scale from one property to a portfolio with confidence

Let’s walk through a practical, expert-informed roadmap on how to budget for a rental property investment in 2025 — without turning this into a PhD in finance.

Step 1: Define Your Investment Goal Before You Touch a Calculator

Most people skip this and jump straight into spreadsheets. That’s backwards.

Are you trying to:

– Maximize monthly cash flow?

– Build long-term equity and net worth?

– Reduce taxes?

– Hedge against inflation?

An experienced investor will tell you: your goal dictates your budget, especially how aggressive or conservative you are with assumptions.

For example, a cash-flow-first investor might:

– Demand a higher cap rate (e.g., 7–9%)

– Use conservative rent estimates and overestimate expenses

While an appreciation-focused investor might:

– Accept break-even cash flow on day one

– Target the best markets for rental property investment with strong job growth and limited supply, even if yields look lower immediately

Write your goal down. You’ll use it to decide if a deal “passes” your budget test or not.

Step 2: Break Down Every Cost — Not Just the Obvious Ones

The Three Layers of Rental Property Costs

Think of your budget in three layers: acquisition, financing, and operations.

1. Acquisition costs:

– Purchase price

– Closing costs (title, escrow, attorney, inspections, recording fees)

– Upfront repairs and CapEx (roof, HVAC, windows, flooring, major updates)

– Holding costs before rent starts (utilities, insurance, property taxes, interest)

2. Financing costs:

– Down payment

– Loan origination fees and points

– Private mortgage insurance (if applicable)

– Ongoing interest and principal payments

Here’s where investment property loan rates matter a lot. A 1% difference in rate can swing monthly cash flow by hundreds of dollars. Experts generally recommend underwriting deals assuming slightly higher rates than currently advertised, to build a buffer.

3. Operating costs:

This is where beginner budgets usually fail.

– Property taxes

– Insurance (including landlord/short-term rental specific riders)

– Property management fees

– Maintenance and repairs

– Capital expenditures (long-term replacements)

– Utilities (if you cover any)

– HOA/condo fees

– Leasing costs and marketing

– Legal/accounting and licenses

– Vacancy (lost rent during turnover)

Professionals often target 35–50% of gross rent as a rough all-in operating expense ratio (excluding mortgage), depending on property type and market. Use this as a sanity check.

Step 3: Use a Cash Flow Model — But Don’t Blindly Trust It

Old-School Spreadsheets vs Modern Tools

You have two main ways to model numbers:

– Manual spreadsheets (Excel/Sheets)

– Software and online calculators

Spreadsheets are flexible and transparent. You see every cell, every formula. That’s why many experienced operators still live in Excel. But they require discipline and a solid understanding of formulas.

Modern tools, including any decent rental property cash flow calculator, speed things up and reduce formula errors. Many now integrate:

– Market rent estimates

– Tax and insurance proxies by ZIP code

– Amortization schedules

– Scenario analysis (interest rate and rent sensitivity)

However, there are trade-offs.

Pros of using calculators and software:

– Faster underwriting of multiple properties

– Less risk of manual calculation errors

– Built-in assumptions for taxes/insurance in unfamiliar markets

– Easy to adjust variables and rerun scenarios

Cons and risks:

– Hidden default assumptions you may not notice

– Over-optimistic vacancy or maintenance estimates

– Dependence on recent comparables that may not reflect downturns

The expert approach in 2025:

Use software for speed and comparison, but validate with your own conservative assumptions and, ideally, your own spreadsheet model. Treat tools as decision support, not decision makers.

Step 4: The “Conservative Assumptions” Checklist

What Experienced Investors Pad — and Why

Professionals know that the future rarely matches the pretty pro forma. So they deliberately inflate certain line items in the budget.

Key conservative practices:

– Use slightly lower rent than optimistic comps suggest

– Assume higher vacancy than the last 12 months (especially in softening markets)

– Bump maintenance and CapEx for older properties or tough climates

– Model higher insurance costs, especially in catastrophe-prone states

– Use today’s or slightly higher investment property loan rates rather than betting on cuts

A typical conservative underwriting framework might look like:

– 5–8% vacancy

– 8–12% for maintenance (older or more complex properties at the high end)

– 8–12% for CapEx on single-family; more for small multis with shared systems

– Full property management cost, even if you plan to self-manage (your time isn’t free)

This is how experts avoid “phantom cash flow” that disappears the moment the water heater explodes.

Step 5: Comparing Budgeting Approaches

Rule-of-Thumb vs Full Underwriting

Investors generally fall into three camps when it comes to budgeting:

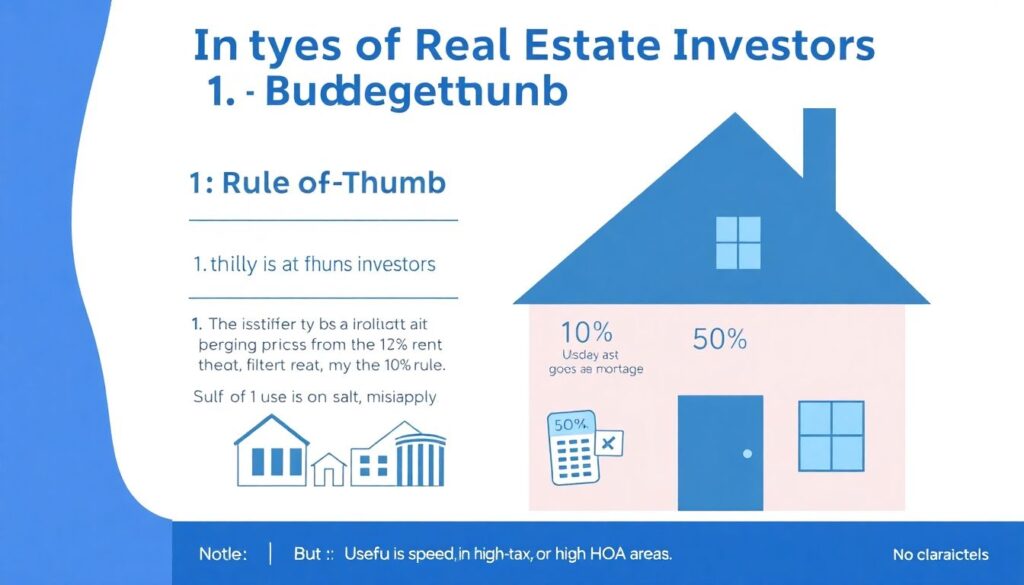

1. Rule-of-thumb investors

They use quick filters like:

– “1% rule” (monthly rent ≈ 1% of purchase price)

– “50% rule” (half of rent goes to expenses, before mortgage)

Useful for speed, but easy to misapply in high-tax or high-HOA areas.

2. Deal-by-deal underwriters

They build a property-specific budget, line by line.

Slower, but far more accurate. This is the professional standard.

3. Portfolio-level planners

In addition to individual property underwriting, they model:

– Aggregated cash flow

– Diversification by market and asset type

– Reserves requirements across all properties

For your first few deals, experts strongly recommend the second approach: detailed, deal-level budgeting. Once you have more units, layering in portfolio-level planning becomes critical.

Step 6: Translating the Budget Into a Buy Box

A solid budget isn’t just a report; it should define your buy box — the exact type of deal you’re hunting for.

That might mean:

– Minimum projected cash-on-cash return (e.g., 8–12% on conservative numbers)

– Minimum monthly cash flow per door (e.g., $200+ after all expenses)

– Neighborhood criteria (crime, schools, employer base)

– Property age, unit mix, and renovation level

This is where your rental property investment strategy meets math. If a deal doesn’t hit your targets with conservative underwriting, it doesn’t qualify — no matter how persuasive the listing agent sounds.

Step 7: Setting Up Reserves — Your Safety Net

A lot of investors can make a spreadsheet look profitable. Very few budget seriously for reserves.

Seasoned operators often follow these benchmarks:

– 3–6 months of total expenses (including mortgage) per property

– Extra reserves when:

– The property is older than 30–40 years

– You’re in a volatile or seasonal market

– Your personal income isn’t very stable

Reserves aren’t “optional” or “nice to have”; they are a core line item in how to budget for rental property. Treat them as a required cost of doing business, not leftover profit.

Step 8: Expert Recommendations for 2025 Market Conditions

What’s Different in 2025

The 2025 environment for rental properties is shaped by a few big forces:

– Interest and investment property loan rates remain higher than in the ultra-cheap money years, even if not at peak levels

– Insurance premiums are climbing in many coastal and catastrophe-prone areas

– Some Sun Belt and boomtown markets are seeing new supply pressure and softer rents

– Data tools and AI-driven pricing are far more accessible to small investors

Because of these shifts, experienced investors are adjusting their budgets and expectations.

Common expert recommendations for 2025:

– Underwrite deals assuming flat rents in the first 12–24 months, not aggressive growth

– De-risk by focusing on employment diversity and solid local incomes

– Avoid underwriting “perfect occupancy” — model realistic downtime

– Demand better deals to offset higher financing costs; don’t stretch for break-even

In other words, slightly less optimism, slightly more margin of safety.

Step 9: Choosing the Right Tech Stack for Budgeting

Pros and Cons of Budgeting Technologies

You don’t need a Wall Street system to budget well. But smart use of tech can help you move faster and avoid rookie mistakes.

Types of tools you might use:

– Online deal analyzers and rental property cash flow calculator apps

– Property management software with built-in P&L and forecasting

– Personal finance or portfolio tools to track debt, equity, and returns

– Market analytics (rent estimates, vacancy rates, neighborhood stats)

Pros:

– Standardized underwriting across multiple deals

– Easier scenario testing (e.g., “What happens if rent drops 10%?”)

– Centralized data for lenders, partners, and your CPA

– Faster screening of opportunities in multiple locations

Cons / Limitations:

– Garbage in, garbage out: bad assumptions still create bad budgets

– Overreliance on automated rent estimates or out-of-date comps

– Subscription creep: paying for tools you barely use

Most experienced investors in 2025 run a hybrid approach:

A reliable base spreadsheet + 1–2 well-chosen tools for speed and market data, rather than chasing every shiny SaaS platform.

Step 10: Budgeting for Different Market Types

Your budget logic changes depending on where you invest.

Investors looking at the best markets for rental property investment in 2025 usually evaluate:

– Job growth and employer mix

– Population trends and housing supply

– Local regulations (especially for short-term rentals and evictions)

– Property taxes and insurance volatility

Then they adapt the budget:

– High-tax markets → larger tax line item and lower acceptable purchase price

– High insurance risk → extra cushion for rate hikes

– Strict regulation markets → set aside more for legal and compliance

Don’t just copy a budget template from a different state. Local conditions can shift your true expense ratio by 10–15 points or more.

Step 11: Practical Budgeting Workflow You Can Reuse

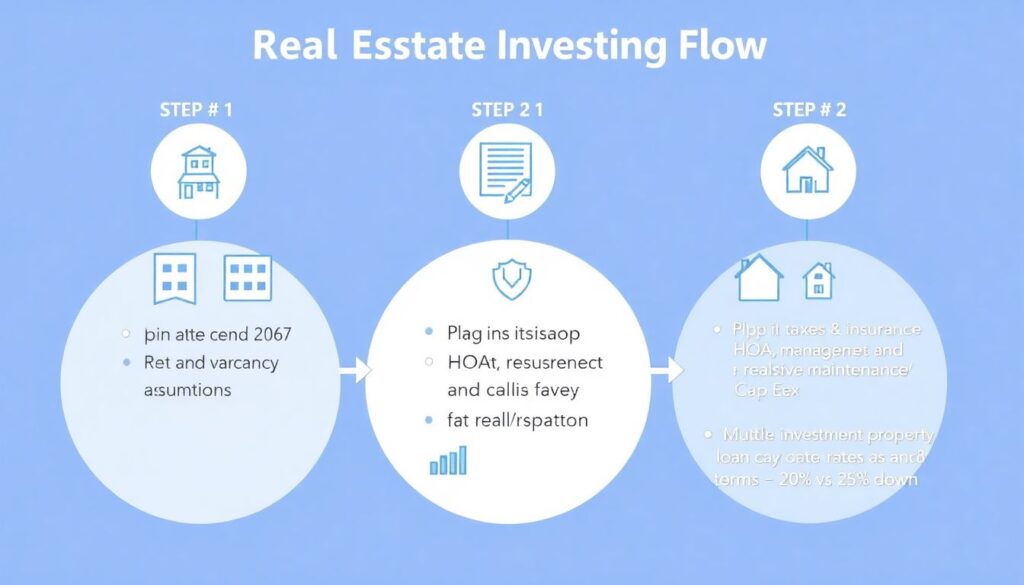

Here’s a simple, repeatable flow that mirrors how many pros operate:

– Step 1: Input conservative rent and vacancy assumptions

– Step 2: Plug in taxes, insurance, HOA, management, and realistic maintenance/CapEx

– Step 3: Model multiple investment property loan rates and terms (e.g., 20% vs 25% down, 20 vs 30 years)

– Step 4: Run best/mid/base case scenarios (e.g., rent ±10%, vacancy ±3%)

– Step 5: Check metrics: cash flow, cash-on-cash, debt service coverage ratio (DSCR)

– Step 6: Compare against your written buy box and risk tolerance

If a deal only works in your best-case scenario, move on. You’re not budgeting; you’re gambling.

Step 12: Common Budgeting Mistakes (and How to Avoid Them)

Short list, but each of these is painful:

– Ignoring CapEx because “everything looks fine right now”

– Underestimating turns, vacancy, or lease-up time

– Forgetting licensing, inspections, and unexpected compliance costs

– Assuming you’ll always self-manage and valuing your time at zero

– Counting appreciation or tax benefits as part of your *monthly* budget

The expert mindset: treat appreciation and tax perks as bonus upside, not something that has to happen for the deal to survive.

Final Thoughts: Budget First, Shop Later

If you build your budget framework before you start scrolling listings, you’ll be far more selective and a lot less emotional.

Summing it up:

– Define your goal and buy box upfront

– Itemize all acquisition, financing, and operating costs

– Use tools and a rental property cash flow calculator, but override them with conservative assumptions

– Stress-test deals for higher rates, lower rents, and higher expenses

– Maintain meaningful reserves and treat them as part of the budget, not an afterthought

Once you internalize how to budget for rental property properly, analyzing a new deal becomes almost mechanical. The emotion goes away, and the numbers tell you whether a property fits your rental property investment strategy — or belongs in someone else’s portfolio, not yours.