From Ledger Books to Algorithms: Why Your Spending Habits Matter in 2025

Короткая история личных расходов

Before phones started nudging us about every coffee purchase, tracking expenses was literally a pen‑and‑paper job. In the 19th century households used ledger books; economists of that era already noticed how small, repeated purchases quietly undermined savings. After WWII, as credit cards spread in the US and Europe, families lost the “pain of paying” cash and overspending accelerated. By the 1990s spreadsheets tried to restore control, but only a minority used them regularly. The real shift began after 2010, when banking APIs and smartphones let apps categorize transactions automatically, turning everyday spending data into something you could actually analyze instead of guess about.

Цифровая эра и взрыв данных о расходах

Fast‑forward to 2025: consulting firms estimate that over 60% of consumers in developed countries have used at least one finance app in the past year, though only about 25–30% use them consistently. That gap between trying and sticking with a tool explains why many people still feel broke despite good incomes. The availability of granular card data, geolocation and subscription logs means your financial footprint is more detailed than any paper budget from the past. The challenge has flipped: you no longer lack information, you lack a simple, smart way to turn it into decisions you can live with month after month.

Smart Ways to Analyze Your Spending Habits Today

Разбор месячных паттернов вместо разовых вспышек

If you want to know how to analyze monthly spending habits, think in terms of patterns, not isolated splurges. One month of data is like a single frame from a movie: mildly interesting but incomplete. Aim for at least three to six months, so you can see which costs are stable, which drift upward, and which spike around holidays or stressful periods. When you average several months, your true “normal” emerges, and emotional distortions fade. This approach also reveals lifestyle creep: that quiet increase in food delivery or ride‑hailing that often hurts more than any one‑time gadget purchase.

Категоризация, которая реально помогает, а не усложняет

Most people either over‑complicate categories or keep them so vague that analysis becomes useless. A practical middle ground is five to eight main buckets: housing, food, transport, health, subscriptions, leisure, and “other”. Within them you can track finer sub‑categories only where it might change your behavior, like separating groceries from restaurants. Historically, economists looked at broad consumption groups; now, thanks to card metadata, algorithms can auto‑tag merchants in seconds. Your job is not to build a perfect taxonomy but to choose labels that answer a simple question: “If this number went up by 20%, would I change something?”

Использование коэффициентов вместо голых сумм

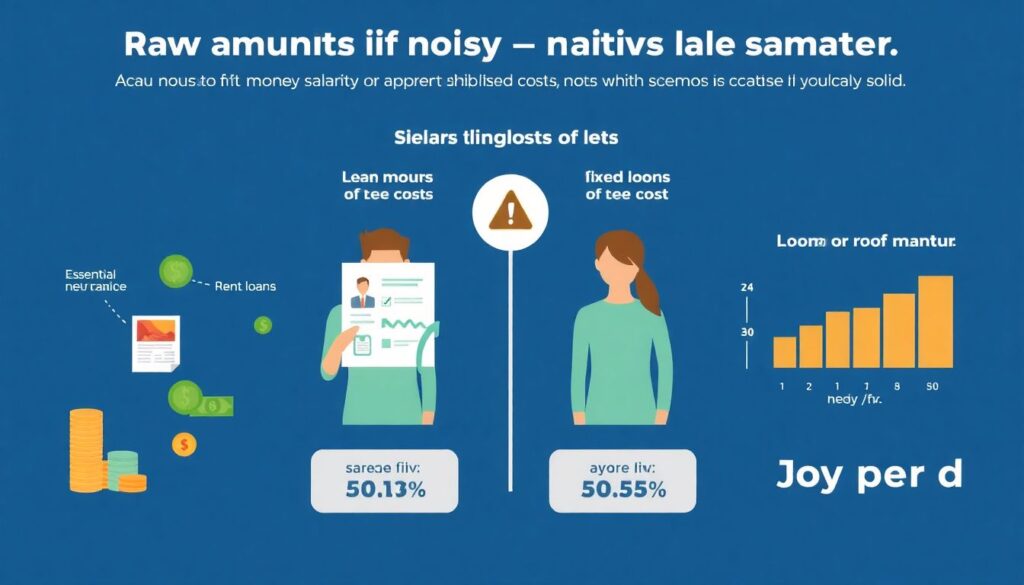

Raw amounts are noisy. Ratios are smarter. One key indicator is the share of fixed costs in your net income: rent, loans, utilities, essential insurance. If those exceed 50–55%, your room for maneuver shrinks dramatically, even if your salary looks solid on paper. Another useful metric is “joy per dollar”: pick two or three categories that give you the most satisfaction and protect them, while being ruthless with low‑joy, low‑necessity spending such as forgotten subscriptions. Historically, household surveys focused on absolute amounts; in the age of volatile incomes and gig work, proportions tell a clearer story about resilience.

Технологии, которые меняют анализ расходов

От тетради к приложению‑наблюдателю

The leap from notebooks to the best budget apps to track spending is not just about convenience, it’s about behavioral feedback. A notebook scolds you only when you open it; an app can send real‑time alerts the moment your restaurant budget is nearly gone, or when subscriptions quietly renew. Since around 2018, machine learning has gotten good enough to predict your end‑of‑month balance based on mid‑month behavior, essentially warning you days before you hit overdraft. This continuous, low‑friction feedback loop is what handwritten budgets never achieved, no matter how disciplined the person with the pen used to be.

Инструменты личных финансов как мини‑лаборатории поведения

Modern personal finance tools for tracking expenses act like small behavioral labs in your pocket. They test which nudges work: a graph of weekly spending, a comparison with last month, or a reminder about upcoming bills. Studies done around 2022–2024 show that users who receive personalized, timely prompts cut avoidable spending by 5–10% without feeling deprived. By 2025, many banking apps integrate these features natively, blurring the line between “bank” and “coach”. You’re not just tracking what happened; you’re quietly training your future self to anticipate pitfalls before they occur, guided by your own historical data.

Выбор приложения под ваш характер, а не по рейтингу

The best expense tracker app for managing budget is the one you will still open three months from now. Some people need detailed charts and export to spreadsheets; others only want a daily “traffic light” showing green, yellow, or red versus plan. Personality matters: if you hate data entry, choose tools that auto‑sync with bank accounts and cash‑flow projections. If privacy is crucial, opt for apps that work offline and let you store encrypted backups locally. The key is to reduce friction; the lower the effort, the higher the chance your tracking turns into a habit and not a short‑lived experiment.

Онлайн‑сервисы для управления финансами в эпоху подписок

With the subscription economy in full swing, online budgeting software to control spending has become almost a necessity, not a luxury. Streaming, cloud storage, fitness, apps, newsletter memberships: each seems tiny, but together they form a significant chunk of monthly outflows. Smart software now scans for recurring charges, flags price increases, and estimates your annual cost of “everything you forgot you pay for”. This function barely existed a decade ago because the market for subscriptions was smaller. In 2025, taming this quiet leak is one of the fastest ways to free up cash without changing your visible lifestyle too drastically.

Экономические и индустриальные последствия

Почему микрорешения домохозяйств волнуют макроэкономистов

On an individual level, better spending analysis means fewer late fees and more savings. Scaled up, it reshapes economies. Central banks and research institutes rely on anonymized card and app data to understand how households react to inflation or rate hikes almost in real time, something impossible with old paper surveys. When millions of people shift money from impulse shopping to emergency funds, consumer cycles smooth out slightly, making recessions less brutal. This doesn’t eliminate downturns, of course, but it moderates extremes. In that sense, your quiet decision to track expenses influences demand patterns far beyond your own bank account.

Прогнозы: куда движется индустрия анализа расходов

Analysts expect the market for consumer finance apps and analytics to keep growing by roughly 12–15% annually through 2030, driven by AI‑powered forecasting and deeper bank integrations. By 2028, your main finance app may operate more like an autopilot, automatically categorizing, predicting, and even negotiating some bills, while you approve scenarios rather than individual payments. Biometric logins and privacy‑preserving tech should also mature, letting apps learn from your history without exposing raw data to third parties. The long‑term trend mirrors the old dream of 19th‑century budget manuals: a stable household, just now with algorithms instead of ink and paper.

Как меняется финансовая индустрия под давлением пользователей

Widespread adoption of smart tracking pushes banks and fintechs to be more transparent. Hidden fees are harder to hide when apps highlight them in red and suggest cheaper alternatives. Some neobanks already build best budget apps to track spending into their core offer to win sticky customers. Insurers experiment with pricing based partly on spending patterns that correlate with financial stability, while regulators debate how far such profiling should go. Traditional institutions that once thrived on customer confusion now face a marketplace where people can compare options with a few taps, guided by the same data they use to know themselves.

Личный выбор как элемент финансовой устойчивости общества

In 2025, analyzing your spending habits is no longer just a self‑help project; it’s part of a broader shift toward financial resilience. Households with clear budgets and at least three months of essential expenses saved are better able to handle shocks like layoffs or medical bills, reducing strain on social safety nets. As more citizens use an expense tracker app for managing budget decisions, societies gain a buffer against crises triggered by over‑leveraged consumers. Behind every neat graph in your app lies a very old idea from economic history: those who understand their daily money flows are freer to plan their future, instead of being dragged by it.