Map your starting point and set shared definitions

Begin with a calm inventory: income streams, fixed bills, variable spending, debts, credit scores, and any hidden subscriptions. Name accounts and owners, then define what “ours” means before arguing about numbers. A simple prompt—how to combine finances after marriage without losing autonomy—frames the talk. Case: Maya earned on commission, Leo had a salary; listing cashflow showed why his paycheck could anchor essentials while hers fed savings. Pro tip: write a one-page money charter with goals, deal-breakers, and a protocol for surprises over $200. Warning: skipping credit reports often hides rate-killing errors.

Choose the structure that fits your personalities

Decide on a model before picking tools: full merge, partial merge, or parallel systems. The classic debate—joint bank account vs separate accounts marriage—has no universal winner; it’s about trust, transparency, and cognitive load. Case: Alicia and Tom fought less after switching to a “Yours, Mine, Ours” setup: joint for rent, groceries, insurance; personal accounts for hobbies. They automated proportional contributions based on income. Pitfall: 50/50 splits can feel unfair when incomes differ; consider proportional funding to reduce resentment and keep motivation intact.

Open the right accounts and label the money

If you run a joint hub, look at low-fee options, ATM access, and sub-accounts for clarity. Many banks let you nickname buckets—“Mortgage,” “Vacation,” “Emergency”—which boosts follow-through. Research the best joint checking accounts for couples with automatic bill-pay, overdraft protection that doesn’t snowball, and real-time alerts. Case: Priya and Evan avoided late fees by auto-paying utilities from the joint account while keeping individual cards for personal spend. Warning: don’t mingle business revenue; keep separate business banking to protect taxes and legal boundaries.

Stand up a budget that adapts in real time

Build a monthly plan anchored to goals: emergency fund first, then debt payoff, then investments. Use the best budgeting apps for couples that sync across devices, tag shared vs personal transactions, and display category trends. Case: Nina and Jorge set weekly “money sprints” of 15 minutes, reviewing app dashboards on Sundays; their grocery overages dropped by 18% in two months. Tip for beginners: start with three big categories—Essentials, Goals, Fun—then refine. Avoid obsessing over coffee; target the top three spend drivers for faster wins.

Automate cashflow and safeguard the essentials

Route paychecks predictably: direct deposit to the joint account for core bills, then scheduled transfers to savings and personal spending. Automate contributions the day after payday to remove temptation. Case: Devon, a freelancer, created a “tax skim” sub-account set at 25% of inflows; quarterly estimates stopped being a crisis. Add buffers: one month of expenses in checking reduces overdraft risk. Warning: stacking payment due dates on the same week of the month strains liquidity; stagger them with billers to smooth outflows.

Tackle debt strategically and protect your credit

List debts by interest rate and type; refinance or consolidate only if fees don’t erase gains. Agree on rules for co-signing and authorized users. Case: Serena’s credit score dipped when her partner maxed a shared card for a surprise trip; they recovered by lowering utilization under 30% and adding a small installment loan to diversify credit mix. Beginners’ tip: pick one payoff method—avalanche for math, snowball for motivation—and stick to it for six months. Keep emergency funds separate from debt payoff to avoid relapsing.

Invest together and align on risk and timelines

Translate goals into accounts: 3–6 months in cash, then retirement accounts, then taxable investments for mid-term aims. Calibrate risk tolerance jointly; the calmer partner shouldn’t be the only brake. Case: Omar wanted aggressive stocks, Lina preferred stability; they split portfolios by horizon—retirement tilted to equities, home down payment in short-term bonds. If unsure, a quick search for a financial advisor for couples near me can surface planners who do flat-fee sessions. Warning: chasing hot tips creates whiplash; use an investment policy statement.

Insure intelligently and update legal documents

Revisit health, life, disability, and renters/home policies; marriage changes optimal coverage. Name beneficiaries on retirement accounts and add transfer-on-death to relevant assets. Case: A minor beneficiary stalled a payout; parents updated to a testamentary trust, preventing a repeat. Establish powers of attorney and a simple will; it’s unglamorous but crucial. Tip: employer life insurance is cheap but often insufficient; get a level-term policy aligned with mortgage and income replacement needs. Avoid whole-life unless a planner shows a clear, tax-efficient rationale.

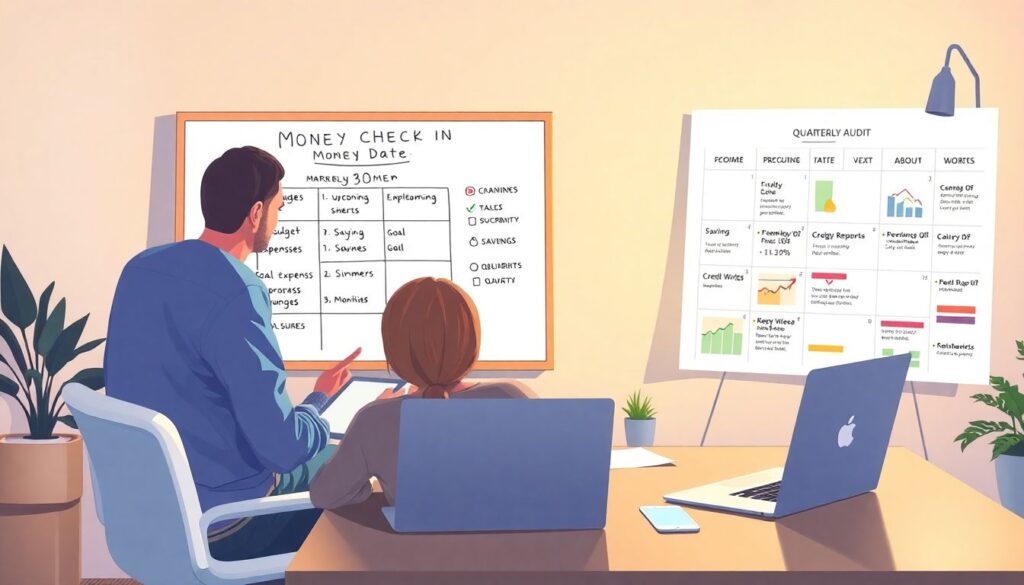

Run monthly mini-reviews and a quarterly deep dive

Set a 30-minute monthly check-in with a predictable agenda: budget variance, upcoming expenses, goal progress, and any simmering worries. Every quarter, run a deeper audit: subscriptions, savings rates, credit reports, and net worth. Case: By treating the meeting like a calendarized “money date,” Kai and Ruth cut conflict, because decisions lived in a ritual, not in random texts. Red flag: secret accounts for non-safety reasons erode trust; instead, create judgment-free personal spends within agreed limits. Celebrate small milestones to reinforce the habits.

Common pitfalls and beginner safeguards

Big mistakes cluster around silence, speed, and scope: couples merge too fast, skip documentation, or ignore emotional triggers. Start slower than you think: pilot the system for two pay cycles before going all-in. Keep receipts and shared notes in one cloud folder; future-you will thank you at tax time. Case: After a rushed merge, Jo and Max double-paid a loan; a two-step approval rule would have caught it. Remember, the “best” system is the one you’ll maintain—tools matter less than routines and trust built week by week.