Becoming a parent flips your financial world overnight. Insurance stops being an abstract “later” topic and turns into a safety net for a very real tiny human. Below is a practical, expert-backed guide to help you sort out what to buy, what to skip, and how to avoid overpaying while your budget is already under pressure from diapers and daycare.

—

Core concepts: what “insurance planning” really means

Insurance planning for new parents is the process of identifying financial risks (early death, disability, major illness, hospital bills) and transferring part of those risks to an insurer in exchange for a premium. In expert language, your goal is to protect your human capital (будущий заработок) and cover liability exposures (obligations like mortgage and child expenses). Instead of chasing every product on the market, you build a set of coordinated policies that match your family’s cash flow, time horizon and risk tolerance.

Key terms you’ll actually use

Before comparing options, it helps to decode the jargon. Premium – the amount you pay the insurer, monthly or annually. Coverage amount (face amount) – the sum your beneficiaries receive if the insured event happens. Beneficiary – the person who gets the payout, usually the other parent or a trust for the child. Rider – an add‑on that modifies a base policy (for example, child rider or disability waiver). Experts recommend reading the policy illustration, not just the brochure, to see projected premiums, benefits and built‑in assumptions.

—

Life insurance: protecting income, not chasing investments

Why life insurance is non‑negotiable for new parents

When one parent dies, the main financial shock comes from lost income and increased childcare costs. Life insurance for new parents is essentially a contract that converts that risk into a lump‑sum payment. Professional planners calculate the needed coverage as: Needed coverage = (Years of income replacement × annual expenses) + debts − existing assets. For most young families, that ends up several times higher than their current annual income. The idea is not to “beat the market”, but to give the surviving parent time to stabilize without panic decisions.

Term vs permanent: what experts choose for themselves

Most independent financial planners favor term life for young families because it buys a large coverage amount for a low premium. Term life covers you for a fixed period (say 20 or 30 years) and then expires. Permanent life (whole, universal, indexed) includes a savings element and lifelong coverage, but at several times the premium. In practice, the best life insurance policy for young families is usually a simple 20–30‑year level term policy that covers the years until the youngest child is financially independent and the mortgage is mostly paid down.

—

How much and how long: sizing your life insurance

Step‑by‑step coverage calculation

Experts often start with the “DIME” model: Debt, Income, Mortgage, Education. You total short‑term debts, estimate how many years of income your family would need, add the remaining mortgage balance and projected education costs. Then subtract liquid savings and existing coverage. That net amount becomes your target face value. It’s more precise than random rules like “10× income”, but still simple enough to do on a notepad. As your salary, debts or number of children change, you repeat the calculation and adjust policies instead of guessing.

Choosing term length like a project manager

Think of term length as a timeline of obligations. Map major milestones on a simple text diagram:

Child age: 0–––5–––10–––15–––20–––25

Events: daycare – school – college – first job

Align your life insurance duration so that it spans until the latest major dependency (usually end of college or mortgage term). If you plan another baby soon, add a buffer of 5–10 years. Experts often recommend laddering two terms, e.g. one 20‑year and one 30‑year policy, instead of a single huge policy, so parts of coverage drop off as your obligations shrink.

—

Shopping smart: quotes, underwriting and common traps

Using term life insurance quotes for new parents

Online comparison tools are useful, but they only show illustrative premiums. Underwriting still depends on age, health, occupation and lifestyle. Collect term life insurance quotes for new parents from at least three high‑rated insurers, checking for: guaranteed level premiums, convertibility options, and clear exclusions. Experts advise locking in coverage early in your 20s–30s, because even small health changes (elevated blood pressure, higher BMI) can move you into a worse risk class and increase lifetime premium costs far more than the price of starting today.

Red flags and sales tactics to resist

Several patterns worry professionals: oversized permanent policies sold as “retirement plans”, policies with complicated bonuses hiding high fees, and riders you don’t understand but still pay for. Another trap is relying solely on employer‑provided coverage; it’s usually limited and not portable if you change jobs. Independent fee‑only planners recommend a clean structure: individual term policy as the backbone, employer coverage as a bonus. If an agent cannot explain all costs, commissions and surrender charges in plain language, treat that as a warning signal.

—

Health insurance: protecting against medical shocks

Why newborn coverage is time‑sensitive

Hospital stays, pediatric visits and vaccinations generate a sharp cost spike in the first year. Family health insurance plans for newborn baby care are designed to integrate maternity, neonatal treatment and continuing pediatric coverage. In many countries, there is a narrow enrollment window (often 30–60 days after birth) to add your baby to an existing policy without medical underwriting. Missing this window can force you into more expensive, less comprehensive options. Specialists advise contacting your insurer during the third trimester to pre‑fill forms and avoid administrative delays.

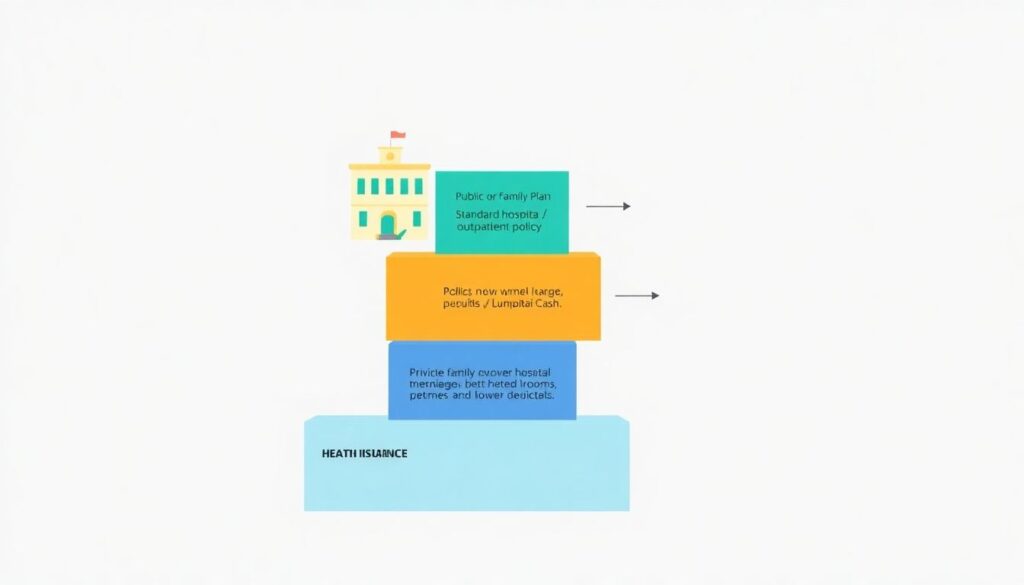

Diagram: structuring your family health coverage

Visualize your setup as layered blocks:

[Base layer: public or employer plan]

→ covers standard hospital and outpatient services.

[Second layer: private family policy]

→ adds better networks, private rooms, or lower deductibles.

[Optional layer: critical illness or hospital cash]

→ provides lump‑sum payouts for major diagnoses or long stays.

This text diagram helps you see overlaps and gaps: if the base plan already offers robust pediatric care, you might skip certain riders and redirect premiums to life or disability coverage instead.

—

Beyond life and health: filling the real‑world gaps

Disability and income protection

For a young household, the probability of long‑term disability is statistically higher than early death. A disability policy replaces part of your income if illness or accident stops you from working. Occupational definitions vary: “own occupation” policies are more protective but pricier than “any occupation” ones. Experts typically prioritize disability insurance for the main earner, especially in single‑income families. Short‑term sick pay from an employer rarely covers extended recovery, so a dedicated long‑term disability plan becomes a critical part of the family risk‑management architecture.

Liability and property protection for parents

With children, liability exposures expand: home visitors, playdates, and online activities. Solid homeowners or renters insurance, with high enough liability limits, protects against accidents on your property. Umbrella liability insurance adds another layer of coverage above those limits at relatively low cost per million of coverage. While less emotionally charged than baby‑focused products, these policies prevent one lawsuit or major accident from derailing education savings or forcing the sale of your home. Experts view them as a cost‑effective complement to life and health insurance.

—

Integrating insurance into broader financial planning

From isolated policies to a coherent strategy

Policies should not exist in a vacuum. Financial planning and insurance services for young families aim to coordinate your emergency fund, debt repayment, investing and insurance into one roadmap. The usual expert sequence is: build a 3–6 month emergency fund, secure adequate term life and disability coverage, then start regular investing for retirement and education. Insurance protects the plan from catastrophic shocks; investments grow your future options. Reviewing this setup every 1–2 years, or after big life events, keeps it aligned with your evolving family structure and income.

Beneficiaries, guardians and simple legal setup

Even the best policy fails if the payout cannot reach your child efficiently. Name primary and contingent beneficiaries, and update them after marriage, divorce or additional children. For minors, many estate attorneys recommend using a simple trust or custodial account instead of naming the child directly; otherwise, courts may need to appoint a guardian before funds are released. Coordinating beneficiary designations with a basic will that names a guardian creates a clear legal pathway from insurance payout to your child’s daily support and long‑term needs.

—

Practical expert tips for new parents

Checklist you can act on this month

– Calculate your coverage need using the DIME method instead of guessing.

– Get at least one standalone term policy outside your employer.

– Add your baby to your health plan within the allowed enrollment window.

– Set up or update your will, guardianship wishes and beneficiaries.

These steps create a functional baseline. Once in place, you can refine product choices, but your family is not exposed to catastrophic risk in the meantime.

What professionals do differently

Advisers who are also parents tend to follow several consistent habits:

– They choose term over complex permanent products early on.

– They prioritize disability and health coverage alongside life insurance.

– They review all policies after each birth, job change or major loan.

When discussing life insurance for new parents or searching for the best life insurance policy for young families, they focus less on brand names and more on transparent contracts, strong insurer ratings and flexibility to adjust coverage as family life inevitably evolves.